Annual letter 2022

The purpose of this yearend review is to share some of our learnings over the past year; rub our noses in our mistakes and to suggest some ways in which we can improve. We start with an overview of the year. Then we move on to review the positions we sold – there were a lot of mistakes – and to briefly cover the thesis of our currently portfolio. Next, we critically analyse how our businesses did in 2022. Finally, we will conclude by expressing some of our goals and thoughts for the next year.

We highly recommend reading the PDF version of this article with graphs and images.

A Year of Change

“Like all financial panics, the signs had been there to see—but no one bothered to look until it was too late”

- David Nasaw, “Andrew Carnegie”

2022 was a year of change both for the world at large and for White Loch Capital Management. War returned to Europe after an age of peace; interest rates increased after decades of falling; inflation reared its ugly head after laying dormant for a generation; a Bear market ended the longest Bull market in US history (neglecting the Covid blip). This truly was a year of change - or a year of mean reversion. 2022 felt nothing like the 2021 euphoria. Despite the doom and gloom, we welcome the changes in monetary policy, we have long felt that the easy monetary policy has led to bad capital allocation and the golden era of fraud – which we hope is finally coming to its cyclical apogee. FTX, Dogecoin and “GameStonk” are just a few symptoms of the underlying rot that has festered because of Modern Monetary Theory. Loose monetary policy caused capital to be diverted away from real projects that would generate returns for society and investors alike, into speculative companies/projects with roulette like odds of a positive outcome. This has a genuine cost for society. We foresee a long hangover, many “Zombie Companies” still wander among us, draining society’s resources. However, we remain optimistic that on the other side society will be healthier and better capital allocation may usher in a period of higher global growth.

One consequence of the increased uncertainty and the change in monetary policy has been investors at large shortening their time horizon. This is part of the explanation behind the steep sell off in “Growth” stocks, even those that we felt were not excessively overvalued. Like bonds, equities can be categorised into short-dated or long-dated securities depending on when cashflows are likely to occur. Short-dated equities where most of their value is derived from near term cashflows are, like short-dated bonds, less affected affected by higher interest rates and there is generally less uncertainty in estimating the cashflows. Many investors have been driven out of long-dated equities and into the safety of short-dated equities. As natural contrarians we are trying to extend our time-horizon during a period when everyone else is shortening theirs. One reason that we can have a long time-horizon is that we are investing in companies with the “Capacity to Suffer”. We feel that our companies have the management teams and balancesheets in place to not only weather any downturn but to take advantage of it.

We are picking through the rubble looking for high quality, advantaged businesses, which have been thrown out alongside all the speculative “Growth” companies. One thing that has surprised us is despite companies being down 80%/90% how overvalued a lot of stuff still is – Rivian down 80% still trades at 14x sales, Shopify down 70% trades at 9x sales. It really puts into perspective how euphoric things got in 2021. While the speculative stuff will probably never make sense to us, we are finding many cashflow positive companies that seem to have been taken out alongside the rubbish - particularly in European small-caps. European small caps have been out of favour for a long time and entered 2022 undervalued and exited even more so, on a relative and absolute basis. Taking a simple index approach, we can see that over the last 5 years European small caps have averaged an annual return of less than 2% and have an average PE ratio of 13x vs nearly 19x for North American stocks. We get are getting excited by the opportunity set in European small-caps and are going to focus our attention on researching companies in this fertile hunting ground.

There as been a sea of change at WLCM over the last year, we have sold 5 positions during the year and purchased 3 – more details later. This resulted from mistakes made and an evolution in our investment philosophy. Coming out of the Covid crash in March 2020 we had a barbell type of portfolio many small speculative positions – like Dananos Corp, Empire State Reality Trust, Global Cord Blood (now in liquidation) - and then a few big positions in stalwarts like Coca Cola and Tyson Foods. We found that, even with the small position sizing, the speculative investments did not sit well with us because we did not truly understand the businesses. It did not pass the “Sleep Test”. We did well on our speculative stuff coming out of the Covid crash but we sold out and moved on. It is not an area we feel comfortable playing in. We have since moved onto looking for Compounders with long growth runways which naturally leads us to seek out advantaged businesses that we feel we utterly understand and are led by trustworthy management. Coming into 2022 our portfolio of mainly big stalwarts was, in our opinion, substantially over-valued while the market around them crashed. We saw this as an opportunity to buy into some of the smaller businesses we had been studying and knew intimately. The businesses we bought had fallen 30% - 50% from all time highs representing what we thought was excellent value. In the process we experienced the pain of trying to catch a falling knife, with some of our buys falling a further 30%/40% before bottoming. Our view is that we are unable to time the market or even come remotely close to predicting when a stock will bottom. We are happy with the businesses we own at the price we bought them. With this act of knife catching WLCM ended the year down 14%.

Portfolio

“Long duration businesses. Long duration ownership. Long duration relationships.”

- Jake Taylor

At WLCM we are looking to own a concentrated portfolio of companies that can compound wealth at above average rates for long periods of time. So, the fact that we sold 5 companies this year is a big disappointment for us. We made a lot of mistakes. We have so many mistakes to deal with this year that we will only briefly discuss them here, we may in the future write a full post-mortem on the ideas.

What we have found over the years is that our “Sleep Test” is a function of how well we understand the businesses we own and how well they satisfy our Compounder Framework. It is not a function of how well diversified we are or the market cap of the businesses. We sleep very soundly at night with our contracted portfolio of Compounders. Much better than we would with a large portfolio of companies we did not understand. More information about our Compounder Framework can be found here

Businesses we sold

Coca Cola (KO)

Coca Cola is a well-run company whose competitive advantages are well known. We liked the fact that they were concentrating their efforts into their bigger brands and divesting many of their auxiliary brands. We also thought that as markets like China and India continued to develop, they would consume more Coke products and would allow Coke to grow at rates above world GDP growth. By the start of 2022 as many investors were turning defensive stalwarts Coke got, in our opinion, relatively overpriced and we found better places to put the money.

Posco ADR (PKX)

We got interested in Posco because we thought it had the best steel business in the world alongside some interesting subsidiaries, especially the Posco Chemical. We strayed outside our Circle of Competence. We were wrong on Posco. We thought capital allocation at Posco was not sensible, pouring money into lithium mining during peak lithium prices, just as Tesla stock was skyrocketing. We also realised no matter how much we studied the steel industry or how many conferences attended we were never going to be an expert in a field where you need to be an expert. We left the investment after 3 years with a great deal of humility, some knowledge about electric arc furnaces and a slight profit. The biggest learning from Posco is to avoid competing in fields that are filled with incredibly smart experts and in companies where you really need to be right about the commodity. With Posco we really needed to be right on steel, the other businesses though interesting, did not matter too much.

Tremor International (TRMR)

Initially this business got us overly excited because of how cheap it seemed. We bought a small position during the middle of 2022, roughly 1% of the portfolio. We believe you truly learn about business as an owner. We quickly learned we did not trust management. Doing some digging we found that CEO Ofer Druker had set up 3 malicious adware computer programs (basically computer viruses) and had been forced out by activists at his last firm Matomy Media Group for empire building. When put into this context the cash on Termor’s balance-sheet could not in our opinion be valued as cash because Druker was either going to waste it on empire building or it would end up in his own pocket. We sold out very quickly, within a month. We have learned from previous mistakes not to get over excited when we see something that looks like a cinch and are proud that we started with a tiny position. We want to continue to slow down our decision-making process even more and really let our System 2 Brain work. In this case our initial position was a mistake but due to position sizing and industrious research we managed to identify our mistake quickly and no harm was done.

Tyson Foods (TSN)

On the face of it we liked Tyson Foods, founding family involved, solid balance-sheet and business, with the secular tailwind of ever-increasing protein consumption. Witnessing Tyson’s international expansion first hand in China, where Tyson was filling the shelves in the rapidly growing HeMa supermarkets, may have also biased our perspective. Its international segment remains a small segment with poor margins. Over the years of owning this business we thought that there were real problems with management, and they could not get it right – though Donnie King is an improvement on previous outside hires. It is an awfully hard business to run. We also began to realise that the increased automation that Tyson has long talked about would probably not be margin accretive as competition would soon adopt similar cost saving technologies. The consumer would be the winners not the companies. With our opinion of the business and controlling family deteriorating we decided to take advantage of the high prices in defensive companies and sell at the start of 2022.

Vestas ADR (VWDRY)

We sold Vestas right at the end of 2022, just before starting to write this letter. This is an example of where we were simply wrong on the business. Our original thesis was that Vestas would end up with a similar model to companies like OTIS where most of the money is made in servicing the products. Vestas has a hugely profitable service segment with average contract durations of over 10 years, with built in inflation protection. We really like the service business and still do. However, it became clear to us that management were not going to prioritise the service segment and that being a windmill manufacturer was the focus of the company. The windmill business is a tough one with many competitors, and an undifferentiated product. The main competition in the future will come from cheaper Chinese manufacturers like GoldWind. It is not clear to us that Vestas will earn high returns on capital by focusing on windmill manufacturing. We also recognised that even if managements’ profitability goals could be met that the company was not trading cheaply compared to the opportunity set. We exited having learned a lot. Currently the money invested in Vestas is sitting in the portfolio as cash, we usually do not like having cash in the portfolio, we view it as inherently trying to time the market, but we do not feel like there is any sensible place to put it currently. Although a lot of European, especially Polish, companies have our attention.

Businesses we Bought

Marlowe Plc (MRL.LSE)

We bought our small position in Marlowe in the middle of the year. It was brought to our attention as we went through the list of serial acquirers at end of the fantastic book on serial acquirers at: https://www.acquirers.com/serial-acquirers . Marlowe is British founder run serial acquirer operating in the highly fragmented UK regulatory compliance and safety assurance markets. Marlowe has acquired businesses at a furious pace – 76 since 2017 - to buy and build a “one-stop service” for all a business’ compliance needs. We feel that by aggregating the best of class solutions Marlowe is building a competitive advantage, which will be hard to replicate. Marlowe has been able to acquire businesses for relatively low multiples 6x-8x EV/EBITDA, which seems like a reasonable multiple to us, not magnificent though. Marlowe claims that each acquisition adds more value to the business as it can cross-sell and broaden its offering while cutting costs, brining down the EV/EBITDA paid to 1x. However, we are often skeptical of overly optimistic synergy and cross-selling claims. Over the last 5 years revenue and EBITDA have compounded at an annual rate of 41% and 64% respectively. We reckon that Marlowe’s buying spree is now ending and they have built a unique competitively advantaged business, that management claim can grow organically around 8% a year with EBITDA margins of 20%.

Founder and CEO Alex Dacre is young, only 35, he has already had success at Restore Plc as the head of M&A. It is rare to find someone so young coming so highly regarded. We feel that the Mr Dacre and executive team are highly aligned with shareholders. Dacre owns roughly 5% of the outstanding shares. Dacre along with other executives and directors have been purchasing shares in the open market during 2022. The executive team take, what we feel, is a modest annual salary alongside an Executive Incentive Plan that compensates executives to the value of 10% of total shareholder return between 2021 and 2026 above a 10% hurdle rate, based on a 2021 share price of £6.90. With current share prices around £5, the stock price would need to more than double from here till 2026 for the executives to earn anything from the EIP.

There is a lot more to like about Marlowe than we have discussed in this brief introduction to the company, we have not begun to talk about things like the decentralised culture Dacre is building that should unleash entrepreneurial spirt. However, as we have owned and continued to research this company for the better part of a year, we have come to dislike some aspects of the business and have never had the confidence to make it a full position. First, “the biggie” is that with all the acquisitions the financial statements are very messy, it is hard to discern what the underlying business is doing. Management understandably use many “adjusted” measures but as investors we must take their word for it as we personally feel it is hard to get an accurate picture. Therefore, we put a lot of trust in management.

We were really impressed with management and how aligned they were. However, somethings just do not sit right with us. Management, especially Alex Dacre, seems to have very close ties to the Conservative Party and may have run into some cushy deals. The main financier of both Marlowe and Restore (Dacre’s previous place of employment) is former chairman of the Conservative Party Lord Ashcroft who owns about 12% of the shares in Marlowe. Dacre father Paul Dacre is the former editor-in-chief of the Daily Mail and a well known right-wing Brexiteer with ties to the Conservative party. There have been investigations shown that companies linked to the Conservative party may have been given preferential treatment when it came to receiving Covid testing contracts, one of these companies is Marlowe which was given Covid testing contracts via its wholly owned subsidiary Black & Banton. The UK Conservative Party have been hit with a multitude of allegations of crony capitalism and so we do not give much weight to the allegations that Marlowe got preferential treatment.

Finally, for us to to make this a bigger position we really need to see acquisitions slow down and for management to focus on the “build” part of their “buy and build” strategy. We can foresee that Marlowe can end up with a strong competitively advantaged business in a fragmented market. However, we have our reservations about the company and right now we are happy to leave it at a small position. It may end up that we never get fully comfortable with the business, at which point we will be happy we took a patient approach to position sizing. If we decide to make it a full position, we will post a full thesis before we do so. We aim to make sure that we can clearly articulate our investment thesis before we jump in.

Transact Technologies (TACT)

We think that there is a tremendous opportunity in the stock of Transact Technologies because it got wrongly sold off in the vicious beat down of small caps & unprofitable technology stocks. Digging into Transact an investor will find a highly profitable casino printer business, alongside a quick-service-restaurant point of sale business and a new SaaS-type business that the company is rapidly growing. As Transact has tried to grow the SaaS business it has invested heavily through the income statement making it out as if the business is unprofitable. This is not the case. The market has completely got Transact wrong and has lumped it in with unprofitable technology despite many years of profitability in its legacy businesses. We suspect that the value of the legacy printer business alone far exceeds the current market cap. This is the only one of our current portfolio businesses that we do not consider an enduring Compounder. We think the value of Transact is just too great to ignore and see a catalyst to realising value within a 5-year timeframe either by a spin-off of the legacy businesses – two activist investors have board seats but have not publicly talked about their intentions – or the business as a whole returning to profitability like it did in Q3 2022.

Full Thesis can be found here

Volex (VLX.LSE)

Volex is a leading manufacturer of power cords and data cables. This story started as a turnaround story when the largest shareholder Nathaniel Rothschild, who owns about 25% of the company, took over as CEO and chairman after years of mismanagement. Rothschild has shown his ability as an excellent capital allocator earning remarkably high returns on acquisitions and internal projects – the average having a payback period of under 2 years. Rothschild has placed the company as a leader in fast growing, higher margin, industries like EV charging cables and copper data cables. The turnaround story has played out and the stock has quadrupled since Rothschild took over at the end of 2015. We believe that now the interesting story of being a Compounder with competitive advantages, a long growth runway and an incredible management team has begun. We are incredibly happy to be partnered with such great management who are very aligned with shareholders.

Full Thesis can be found here

Remaining Positions

A2Milk (A2M.ASX)

This investment was a result of seeing the brand in China and being amazed at how customers were willing to pay high premiums for it. The more we learned the more we liked. We are of the opinion that a2Milk is a top FMCG brand, with a capital light business and a rock-solid balance sheet. We suspect that the brand can expand beyond infant formula in China and offer nutritional products that support customers throughout their life cycle. a2Milk has an extremely strong brand, it is a brand that mothers are trusting to provide nutrition to their babies. Trust in the Chinese infant formula market is a top priority after the 2008 Chinese Milk Scandal, mothers are willing to pay high premiums for that trust. We bought a2Milk when they were hit by their first inventory write down due to Covid supply chain disruptions. We quickly made it a full position as the stock continued to drop. Another example of catching a falling knife.

Full Thesis can be found here

Asseco Poland (ACP.WSE)

Asseco Poland is a Polish founder run serial acquirer of software and IT services. Founder Adam Góral has an incredible talent for innovation and vision which has permeated throughout the business. Starting as a Polish ketchup factory, Góral focused on IT systems and software, to transform Asseco into the biggest software developer in Central and Eastern Europe and the 6th biggest in the whole of Europe. Asseco has an extremely strong position in banking and insurance software and IT services. While it has entrenched positions in Poland, Central Europe, and Israel it operates in 60 different countries and has tried to compete in less developed markets. Asseco has steadily acquired businesses over the years building a diverse and decentralised company under their “Federation Model”. In their core business of Banking and insurance software and IT services Asseco has long customer relationships with very sticky recurring revenues. Although they have a great core business, they have expanded beyond that with smaller segments gaining traction such as cyber security, payments, and Cloud solutions.

We think very highly of the CEO and founder Adam Góral who owns nearly 10% of Assseco’s shares. 23% of Asseco’s shares are owned by Cyfrowy Polsat, Poland’s telecommunications leader which is founded by Poland’s second richest person Zygmunt Solorz-Żak, after a strategic partnership was struck between the two companies in 2019. This showed real humility from Góral to let another founder take a bigger position than him, and we can foresee that this partnership may lead to great benefits in the future. We can see that Góral is constantly building for the future and willing to take near-term pain for long-term gain.

Asseco is an exciting business, its core segments have strong competitive advantages and run by a fanatical founder who does not dilute shareholders and trading at a cheap valuation. We liked Asseco a lot when we bought and have only grown to like it more over the years. It has come a long way from ketchup.

Gentex (GNTX)

Gentex is our manufacturer of auto-dimming mirrors. With no debt, high margins, high returns on capital and a monopoly like marketshare there is a lot to like about Gentex. We think that the current management team, who are all young and were all brought up through the company by the founder, have an owner-like mindset. Moreover, management have continued to develop the unique entrepreneurial culture set out by the founder of the business. We believe this unique entrepreneurial culture is what gives Gentex “Spawner DNA”. Originally a smoke detector manufacturer it has continually innovated into new business segments, and we can see the business doing so again. We estimate at current prices this is a Compounder sitting at a reasonable valuation with built-in “free” options on its new innovations. This is a business that the longer we have owned it, the more we like it. Over the years we have steadily increased our position and will probably continue to do so in the future.

Full Thesis can be found here

Hasbro (HAS)

Hasbro is a global toy manufacturer with an incredible portfolio of brands. Our thesis is that Hasbro will be able to leverage its brands particularly its Wizards of the Coast brands. Hasbro could capitalise on its IP that goes way beyond toys. Going forward we will see Hasbro develop more into an entertainment company, using its brands to build out a collection of different game, tv shows and movies. In an era where the consumer is hungry for content and content providers are struggling to keep up, we consider Hasbro to have a strong hand. Building out and creating content will help the legacy toy business where we see it focusing on its own brands and will slowly move away from manufacturing licensed brands. This should over time increase margins and returns on capital in the toy business. It seems competitor Mattel have come out with a similar focus. Despite, in our opinion, having a weaker set of brands Mattel’s management has done the better job of turning its toy business around. Hasbro’s management must do better.

In 2022 Alta Fox announced an activist campaign for change in Hasbro’s board. Alta Fox is a firm that we massively admire and consider Connor Haley an astute investor. As we were reading the material on Hasbro provided by Alta Fox, it gave us confidence that Alta Fox had seen the same value as we had, particularly in the Wizards of the Coast business. However, the Alta Fox campaign showed that we were not doing nearly enough research into board members and management track records. The Alta Fox material showed that we had a huge blind spot in our research process. This was a steep learning curve. Management and directors is now an area that we pay a lot of attention to. As we continue our investment journey, we will continue to make mistakes, but we will get slowly better and better. Part of that journey is learning from incredibly talented investors like Connor Haley.

Despite Alta Fox losing its activist campaign it has done a lot of good for shareholders. Management have increased disclosures around Wizards of the Coast and have started to recognise it is the real value driver of the business. Secondly, we suspect Hasbro’s Brand Blueprint 2.0 has incorporated some of Alta Fox’s views as Hasbro now looks to concentrate on its big brands and to divest its smaller auxiliary brands. We have also seen management continue to sell of parts of the eOne acquisition which is for the best.

How our businesses performed in 2022

“In the most devilishly wicked learning environments, experience will reinforce the exact wrong lessons.”

- David Epstein, “Range”

Analysing quarterly performance may not seem congruent with our long-term ownership mindset. However, we are consistently trying to shorten our feedback loops and focus on how reality is playing out compared to our assumptions. Stock price is an extremely poor source of information with a lot of noise. Over the short-term at best share prices are a distraction at worse they are a mis-leading signal destined to lead investors to making the wrong decisions. Therefore, we seek out better information to update our view on our businesses. We find that the best sources of data are company publications alongside competitor and industry publications. We look purely at how the business is doing in the context of the industry. As if it was a private company.

We think that the thesis tracker over time well help us overcome recency bias. We all too often take what has happened in the recent past and extrapolate it into infinity. This can lead to misjudgment from investors. We may unfairly judge a management team due to their recent performance while discounting too heavily how they performed in the past. The thesis tracker allows us to look back and see how we felt about how the company was performing each quarter. Overtime if we are seeing a lot of reds, we may be giving management too much leeway and it may be worth considering that overconfidence bias or endowment bias is clouding our judgment. Conversely if we are feeling negative about a company and there are a lot of greens on the thesis tracker, we may be just having a difficult day, or some other external factor is clouding our judgment because previously we thought management had been hitting it out the park. The thesis tracker is just another way of giving us more useful data and a way to record our feelings over time. This will only get more useful the longer we use it, especially when used alongside journaling.

a2Milk

Shares of our ultra-premium infant milk formula brand, a2Milk, were up 23% for the year. This is a positive result given the negative sentiment and Chinese boarders remaining closed throughout 2022. In August a2Milk posted their full year 2022 results. After a rough year a2Milk has returned to growth: excluding their acquisition of Mataura, revenue was up 11% for the year but growth accelerated in the second half with sales up 15.7%. Net profit after tax was up 42% and the company ended the year sitting on over NZ$800 million representing about 15% of its market cap. We are encouraged by the performance in the IMF China label which has hit a record high marketshare, with still a long runway of growth ahead of it. We are pleased to hear that a2Milk has initiated a share buyback, at current prices and this will add substantial value for shareholders.

It was also announced that Chairman, David Hearn, will retire at the end of 2023. We do not have strong opinions on this news, but we did find it strange that David Hearn resided in the UK where a2Milk does not do any business and after 9 years on the board of a2Milk we think change is probably a good thing.

Overall, it was a solid year for a2Milk, and we like the direction management is taking the company. The temporary FDA approval to export in the USA, China’s boarders reopening, and new product innovations set up 2023 to be a stellar year for a2Milk.

Asseco Poland

Shares in our Polish IT solutions and software conglomerate, Asseco Poland, fell 14% for the year. Asseco was taken down alongside other technology stocks, however, the shares held up reasonably well because of its high quality, low valuation and high dividend.

Asseco had a year of steady growth. Net profit attributable to the parent company grew by 4% in the first 3 quarters of 2022. This comes off the back of a strong 2021 where profits were up 14%. Asseco Poland is a business we expect moderate growth from, they have a strong position in banking and insurance software with a large marketshare in Poland. We do not expect much growth from this segment. However, Asseco is expanding its capabilities through acquisitions into spaces such as cyber security, robotics, and payments where it has early success. We see most of Asseco’s organic growth coming from these new segments. Asseco still seems undervalued given the quality of its earnings, its strong decentralised, entrepreneurial, culture and its small growth segments. Asseco maintains a healthy balance-sheet, does not dilute shareholders, and pays out excess cash to shareholders. It was another good year to be partnered with this great management team.

Gentex

Share in our rearview mirror and digital vision supplier, Gentex, were down about 22% for the year. So far in the year they have experienced a moderated bounce back in sales and each of the 3 quarters reported of 2022 showed revenue growth. Gentex’s margins have steadily declined as costs increase and they maintain prices for customers. Gentex has 90% marketshare in the auto-dimming rearview market, and it is far above the competition. It wants to maintain its spot as supplier of choice to the OEMs. One-way Gentex is expanding its competitive advantage is by being the supplier who is not forcing through price increases during this period of cost inflation. Gentex have gained marketshare this year and are cementing themselves as the player in auto-dimming rearview mirror space. Gross margins dropped from the highs of 40% a couple of years ago down to 29%. Gentex is still highly profitable and is sitting on a heap of cash which allows it to have the capacity to temporally suffer to position itself better going forward. However, we do expect costs to eventually be pushed through and for margins to get back up to the highs close to 40% over the coming years. In the first 3 quarters of the year Gentex repurchased over $90million worth of shares. We would like to see Gentex ramp up its share repurchases. The macro picture is not looking that bright and 2023 could be a tough year for Gentex if there is a deep recession. However, we know Gentex will weather any storm – no debt, high margins and owner-mindset management - and come out better on the other side.

Hasbro

Shares of our global entertainment company, Hasbro, were down 40% in 2022. Hasbro was by far our worst performer. Hasbro’s sales tend to be lumpy depending on the timing of box set and film releases. This year Hasbro has some tough comparisons compared with 2021 but even with that in mind Hasbro’s performance left a lot to be desired. Revenues were down 5% for the 9 months reported but getting worse as the year went on with third quarter revenue down 15%. Hasbro is our most levered company sitting on about $4billion of debt offset by $500million in cash. We would like to see Hasbro pay down this debt fast as it leaves the company vulnerable to shocks and problems with refinancing – especially with the rising cost of debt. We are seeing positive developments at Hasbro and the newly announced Brand Blueprint 2.0 is a step in the right directions. Management plan to implement cost savings, focus on its big brands and a greater focus on the Wizards of the Coast segment. We are still hopeful that management can unlock the true value of Hasbro’s IP. We think shares are currently looking cheap considering how much cash Hasbro has shown it can throw off over the years.

Marlowe

Shares in our regulatory compliance and safety assurance serial acquirer were down 54% for the year and roughly 20% from our purchase price. The first half 2022 results report in November showed Marlowe continuing to acquire small businesses at a fast pace and there were signs that Marlowe may be growing too fast. Reported revenue grew by 66% yet net earnings per share was slightly down YoY. Moreover, Marlowe, who have insisted they will not need another equity raise, have taken on nearly £200million of debt more than a 3-fold increase YoY. This has us slightly worried and a feeling that the company has over-levered itself. Though Marlowe still has ample debt facilities left to tap, we are going to be looking for Marlowe to de-lever and to focus on organic growth over the coming quarters. At WLCM we are looking for strong businesses that have the capacity to take advantage of a crisis. Leverage makes companies fragile vulnerable to shocks. Right now, Marlowe is looking fragile. However, there are some encouraging signs, organic growth looking to be strong averaging 8%. Cross-selling does seem to be valid tactic with over 40% of customers now taking at least 2 of Marlowe’s services. Revenues seem to be sticky, with over 85% of revenues recurring and contracts tend to be multi-year 3+. Finally underlying margins seem to be improving with EBITDA margins (a figure management like, not us) approaching 19%.

Looking into 2023 one word surmises the prospects of the UK economy – depressing. Marlowe mainly serves UK based SMEs who are vulnerable to downturns. While we agree with management that their services tend to be sticky and non-discretionary, that does not help much if their clients close shop. We are happy to have Marlowe at just under a 2% position size. Despite the disheartening 2022 commentary and 2023 outlook there is still a lot to like about Marlowe. We expect management to do better and focus on organic growth. If we see that then I think Marlowe could be multi-decade Compounder. If we do not, this may well be added to our extensive list of mistakes.

Transact Technologies

Shares of our back of the house software and slot machine printer supplier, Transact Technologies, fell 41% for the year and roughly 18% from our purchase price. For the first two quarters of the year, it seemed that management were being over optimistic, promising cost cutting and showing profitability. However, in the third quarter Management knocked it out of the park showing profitability and superb growth in their legacy Casino printer business. Transact really impressed us this year, management set ambitious goals and delivered on them. During the year Transact have expanded their team and are clearly building the foundations for a bigger, software focused, company. Transact have fully wound down their smaller less profitable segments to focus on the Casino & Gaming and Food Service segments. The streamlined and more focused version of the company is clearly paying dividends with high growth in both of its main segments. Transact finished the third quarter with 68% YoY sales growth and 38% growth in back-of-the-house Food Service terminals. We are very bullish on Transact going into 2023 and think if Transact can show consistent profitability throughout the year it’s egregious undervaluation will be clear for everyone to see.

Volex

Shares in our global integrated power solutions manufacturer, Volex, fell 25% for the year and we finished the year on a small gain from our purchase price. Volex continued to deliver stellar results, again proving their capital allocation is exceptional. First half 2023 results showed organic growth of more than 14% helped along by 53% organic growth in the electric vehicle segment. What gets us most excited is that Volex are investing heavily in growth cap ex, with 90% of current cap ex being growth, only 10% is maintenance. Average cap ex has a payback period of 20 months, and the business currently has a ROCE above 20%. It is not only internal projects that are generating a fantastic return, but their average acquisition has also generated a ROI of over 22%. Understandably when you can get these sorts of returns on capital you want to deploy as much capital as possible. This is exactly what Volex has been doing. Volex acquired 10 businesses during the 6 months for roughly $200million. This has required Volex to tap their debt facility. The market seemed to get spooked by the announced increase in debt, however we disagree. Volex has ample debt facilities left to tap, and the more money they can deploy at these incredible high rates of return the better, without of course letting the company become fragile and dependent on the goodwill of financiers.

We are extremely happy to be partnered with this outstanding management team. Going into 2023 Volex may experience some macro headwinds if the global economy tanks. However, Volex has positioned itself to ride the current of secular trends like growth in Electric Vehicles, Data Centres, Medical Devices. Whatever near-term difficulties the macro environment will throw at Volex pales into insignificance compared to the long-term tailwinds.

Looking Ahead

“Habits are the compound interest of self-improvement.”

- James Clear, “Atomic. Habits”

Resolutions

We have several resolutions at WLCM to in an effort to continually improve. Our first and most important is to create a journal entry everyday regarding our businesses or businesses we are researching. We are big fans of journaling and have mainly been doing it on word documents or seeing our DCFs as journal entries. At the end of 2022 Jake Taylor came out with a journaling product specifically designed for investing call Journalytic (Found at: https://journalytic.com/journal). We have been extremely impressed with this product and it seems like a uniquely suited tool for keeping all our investment notes and thoughts in one space. We could not be happier with the product and its free! Our goal is to end 2023 having made at least 1 journal entry every day this year. The longer we journal the more informative and useful it will be. Used in accordance with our Thesis Tracker and our DCF models, which we basically see as a journal entry of our assumptions, we presume we will end up with less noise in our feedback. We constantly strive to improve our decision making.

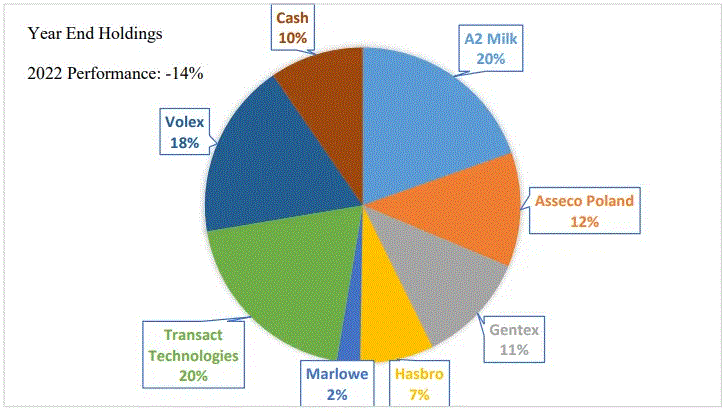

Our other resolution is that we are determined to build out a watchlist with greater depth. During the year we sold 5 businesses, but only felt fully comfortable buying Volex and Transact Technologies from our watchlist. The fact we have 10% in cash and still are not fully confident about Marlowe makes us extremely disappointed in the depth of our watchlist. It will take time to build out a solid “bench” of investments and something we look to greatly improve on in 2023.

Having relocated back to the UK in the second half of 2022, we did not have a lot of time to write. Our goal is to create a weekly, eventually daily, writing habit. We want to write a fully fledged thesis for all of our holding companies and our rule going forward is that we cannot make a “Full-sized” investment before we have written a full investment thesis. This will help our decision making. Writing also has a way of holding ourselves publicly accountable. Employing inconsistency bias to make it more likely we stick to the good practices we have set out in writing.

Some Predictions (just for fun)

Our investment horizon allows us not to look beyond the noise and the short-term macro environment. We are looking to identify long-term secular trends that are giving tailwinds to magnificently run, advantaged, businesses. As an intellectually stimulating exercise we will make some predictions for 2023. We are not in the game of making money from short-term predictions however, they may make us more cautious about investing in certain areas for example our long-held belief that there was a real-estate bubble in China has stopped us investing in companies with exposure to Chinese real-estate. On the same line of thought we now judge there to be a substantial bubble in auto-loans in the USA and UK – perhaps elsewhere but we haven’t seen enough data from other countries to make any judgement. In the USA outstanding auto-loan debt well exceeds $1.5 Trillion with the average monthly payment exceeding $1,000 for the first time in January 2023. A study done by The Car Expert showed that over the last 13 years in the UK the absolute level and average value of auto-loans has increased at a far quicker pace than wages. This has been accelerated by the loose monetary policy incited in 2020. However, the music has stopped. Interest rates around the world are rising, cost of living is increasing, and the average person is sitting with a car too expensive for their wage and a monthly payment they cannot afford.

Alongside real data we have done our own digging and found substantial anecdotal evidence – although not to be relied upon in this case it compliments the data well. In September of 2022 we started doing some boots on the ground research – we needed a new car. Everywhere we went finance was being pushed on us not cars. No one was interested in selling us a car they were interested in selling us finance. A young employee, first job out of school, bragged about selling her previous car for a profit during lockdowns while car prices had skyrocket, she traded up to a £50,000 Audi on finance. Despite, almost proudly, admitting her monthly payments being more than her mortgage, it did not matter because in her mind she was likely to sell the car for more than she bought it for. This was not an isolated incident. The more we asked around the more stories we got like this. The process of buying a car ended up like a scene out of The Big Short where we just could not believe the extent that many people, especially young people, had overextended themselves. Lately the stories have not been so upbeat, and many are looking to rid themselves of this millstone around their necks. The biggest argument for investing in auto-loan companies is that cars are a necessity, and that people will refuse to give up their car. We agree to some extent however, we can foresee many people downgrading cars or switching to public transport as more people are pulled back to working in offices or that people end up with no choice but to default on their auto-loan. We see companies like Credit Acceptance Corp, CACC, as especially exposed to the auto-loans bubble. In our minds companies such as CACC are examples of picking up pennies in front of a steamroller. We will be watching from the sidelines to see if and how it unfolds.

We see China opening up as a positive for the world economy. However, we think there are major fragilities in the Chinese economy and long-term demographic trends that will will mute any rally. We still consider there to be a major real-estate bubble in China that is yet to fully burst. From our 5 years in China, we were astonished by how many empty apartments we saw and how many average people put their life savings into a second or third apartment, not to rent it out but just on the belief that they can profit off the price appreciation. The Chinese government with its absolute control has done well so far to slow the collapse, but we expect the collapse is inevitable, nonetheless. We also predict that going forward China could experience a significant loss of talent. Previously many international Chinese students would aspire to go back to China and work for the up-and-coming Chinese technology giants with a patriotic fervour. However, this completely changed over the last 3 years. Youth unemployment has skyrocketed and even if they can find a job young, educated Chinese face a daunting life in the 9/9/6 work culture, or worse if they choose to work at companies like PinDuoDuo. To make matters worse Chinese entrepreneurism has been almost completely obliterated with violent policy changes, made with deranged clarity, and regular public castrations of China’s most famous businesspeople, Jack Ma, Ren ZhiQiang and even social media influencer Li JiaQi – to name just a few. We have personally seen an exodus of young, educated Chinese moving abroad to escape government controls and the brutal work culture. This prediction comes largely from anecdotal evidence but there has been some data of record emigration levels from Hong Kong.

Next year is likely to be just as unpredictable as any year. However, it does seem that recession is likely to come and that the inebriated ecstasy we experienced in 2021 is unlikely to return. Though we have no real opinion on how likely a recession is or how deep it will be, we feel comfortable with our portfolio of Compounders that have the capacity to suffer. All our businesses are, in our opinion, conservatively financed - a2Milk, Transact Technologies and Gentex having no debt whatsoever. Our companies can be aggressive during times when those around them are in conservation mode. Our serial acquirers, Volex, Marlowe and Asseco Poland, all have ample capacity to acquire more businesses at cheaper prices if there is an economic downturn. We think our companies are in their element during a downturn. At the start of 2022 we spoke with the head of investor relations at Asseco Poland who told us they have struggled to find many proper businesses at reasonable valuations because of the over-exuberance in the market. Many “founders” were coming to them with a PowerPoint presentation and demanding valuations on Price-to-Hope ratios. We are looking forward to a return to sobriety.

White Loch Capital Management is a fictitious fund used for educational purposes only

Thanks for reading

Disclaimer: Do not interpret anything above as financial advice. This article has been prepared for informational & educational purposes only. The writing contains to certain forward-looking statements and opinions which are based on the Author’s analysis of publicly available information believed to be accurate and reliable. While the Author believes that such forward-looking statements and opinions are reasonable, they are subject to unknown risks, uncertainties and other factors that could cause actual results to differ materially from those projected. As of the date the Report is published, the Author may or may not hold a position in the security mentioned. Nothing in this Report constitutes investment advice. Readers should conduct their own due diligence and research and make their own investment decisions. This is NOT a buy or sell recommendation.

Do you still own Asseco? Any interesting writeup that you can share about Asseco? Thanks