Volex ($VLX)

A successful serial-acquirer. Aligned CEO that has a proven track record of great capital allocation. Trading at a significant discount to intrinsic value. Multi-bagger candidate.

Highlights

· A potential multi-bagger

· Successful serial-acquirer

· Incredible capital allocators

· Large insider ownership

· Decentralised owner-mind-set culture

· Operates strongly in highly fragmented markets

· Price is currently offering a substantial margin of safety

We highly recommend reading the PDF version of this article with graphs and images.

Disclaimer

Disclaimer: White Loch Capital Management is a fictions fund that is used purely for educational purposes. The author uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. You are advised to discuss your investment options with your financial advisers, including whether any investment is suitable for your specific needs. Following publication, the Author may transact in the securities mentioned. All expressions of opinion are subject to change without notice, and the author does not undertake to update this report or any information herein.

VOLEX (VLX), SHARE PRICE: £2.65, MARKET CAP £437MM, 15/07/22

Executive summary

White Loch Capital Management believes that, despite the stock almost quadrupling in the last five years, the current market price is offering investors a fantastic opportunity to partner with an already proven tremendous capital allocator, that has transformed what was once an incredibly low margin and low growth business, into a higher margin business positioned as a leader in high growth industries. Volex has strong competitive advantages such as being the low-cost producer, the trusted partner of the industry and one of the only players with truly global scale. Today Volex is a high quality compounder that is aggressively expanding both organically and through acquisition. Volex’s management have shown that they have exceptional capital allocation skills consistently earning incredibly high returns on investments. Volex has implemented a decentralised structure where employees have an owner-mind-set and entrepreneurs are allowed to run their own businesses within Volex. Finally we think the fact that Volex has a long runway ahead of it for growing both organically and inorganically, combined with an incredible management that is aligned with shareholders, where the CEO owns 25% of the company, makes Volex a prime candidate multi-bagger.

History of the Business

Volex is a leader in power solutions with its roots dating back to the 1890s and has been a listed company since 1939. For much of Volex’s history it has been a pioneer at the forefront of the power cord industry and an innovator in product areas such as high-speed data cables. Historically Volex’s products could generally be separated into Power – designing and manufacturing power cords, such as a power cord on a TV – and Data – designing and manufacturing - fibre-optic and copper cables for transferring data such as that seen in a data centre. In the past, the Power division made up about two thirds of the sales and was a very low margin business with gross margins less than 15%. The Data division used to make up only a third of sales and although Volex had some speciality in high value products such as high-speed copper cables this segment also under earned and was mismanaged typically earning only around 20% gross margins. Within these two segments the end customers could broadly be divided up into Consumer electronics – 66% of pre-2016 sales; Telecoms & Data Centres – 17% of pre-2016 sales; Healthcare – 10% of pre-2016 sales and industrials – 7% of pre-2016 sales.

With the growth of cheap Chinese manufacturing Volex’s products began to become commoditised and they were heavily dependent on consumer electronics such as laptops and TVs where large customers such as Apple had massive pricing power. In 2014 Apple accounted for 23% of Volex’s sales and margins for the overall business were consistently below 20% - gross and 1%-2% net. Volex had become a value destroying business, with numerus management teams vowing to turn the business around – from 2008 to 2015 there had been 3 different management teams all with their own turnaround plans. None of which were willing to make the tough decisions necessary such as unwinding the unprofitable business segments and diversifying away from their big customers. Previous management teams could be categorised as centralised, top heavy with a focus on growing revenues over profitability. Factories had become underutilized and by 2015 revenues and margins were tumbling - the future for Volex was looking bleak

The transformation

Having overseen a number of failed turnarounds in November 2015 Volex’s largest shareholder Nathanial Rothschild took over as CEO and Chairman of the board. Since then Rothschild has shown incredible capital allocation acumen and intense customer focus successfully transforming the business into a high-quality serial acquirer that has shaken up the entire cable industry.

One of the first things Rothschild did as CEO was to trim headcount at head office by 40%, something almost unheard of for a business the size of Volex. Rothschild had seen that the bloated top-heavy structure of Volex was compressing margins and leading to bad decision making. Rothschild has implemented a decentralised structure with a tiny executive team that partners with top local managers who have autonomy to run their own businesses and react quickly to the changing environment while at the same time centralising purchasing and fostering cross-selling to capture economies of scale. Rothschild from the very start set out to create a home for businesses where the founder or CEO could still run their own business under Volex’s ownership and creating a culture of long-term Owner-mind-set throughout the whole company with the goal of being the leader in power cords for the next 100 years and beyond.

Next Rothschild set about diversifying their customer base and making the tough decision to unwind unprofitable business segments where large customers had complete pricing power over Volex. This led Volex to apparently offering Apple the Volex factory in Shenzhen, China, that produced power cords for the iPad for nothing, however Apple apparently thought $0 was still too expensive and refused. Despite the Apple business making up 23% of Volex’s sales, $120MM revenues, the business generated no profit. Rothschild shut down the commodity parts of the business and focused on high value-add business segments and investing in intangible assets such as expertise, employee training and other hard to replicate competitive advantages. In 2022 Apple made up less than 2% of Volex’s revenues and made a healthy profit.

The transition took guts, revenues fell, with two years of consecutive declines of 13%, as Volex exited their large businesses all the while the business was burdened with massive amounts of debt – a leverage ratio of 10x EBIT in 2014. Moreover, in 2014 factory utilization rates were abysmal at 52%. Turning Volex around in such a short period of time took an immense amount of work, courage and great capital allocation.

Rothschild has understood that to be the leader in the power cord industry Volex needs to have the largest global reach, the best quality and be the low-cost producer. Volex is well on its way, now having the largest global presence in the industry, with low cost manufacturing sites across 22 countries and 3 continents, Volex has solidified its position as the premium brand attracting customers such as Dyson, Philips and ThermoFisher who have a brand to protect and are only willing to partner with the most trusted businesses. Finally, Volex has started to vertically integrate and are now able to internally satisfy large quantities of their own inputs, including copper. This has widened their moat and put them in an almost unassailable position of the low-cost producer in the industry. Without specifically saying it, Volex is applying the economies of scale share model, popularised by Nick Sleep, as they have said on numerous occasions that long term net margins for the business will stay at between 9%-10% and any cost savings from scale or vertical integration above that target will go towards lowering the price of the product or improving the business through investment in intangibles like employee training or operational efficiency through automation. This makes it very difficult to compete with Volex in their areas of expertise.

Although Rothschild inherited a lot of low margin commodity businesses, he identified areas of the business where Volex had a technological and knowledge based advantage and could generate high margins. This was principally the healthcare and the high-speed data cables business. Focusing on an integrated business model of design & engineer, build and service in areas where Volex have a clear advantage over its competitors has led to a complete change in the business. Today Volex is an undisputed global leader in power solutions for medical devices, AC power cords for electric vehicles, high-speed copper data cables and the largest global manufacturer of consumer electronics power cables. In 2022 Volex boasted net margins of 9% with the goal of getting long term margins to 10%; a leverage ratio of 1.3x EBITDA and achieving high factory utilization rates by implementing automation with Volex now arguably having the industry’s most advanced and efficient factories.

Electric Vehicles

When Rothschild took the helm at end of 2015 the electric vehicle (EV) segment was almost non-existent, however as of 2022 the EV segment accounts for about 17% of revenue and is arguably the most exciting of Volex’s segment experiencing close to a 100% organic growth rate in 2022. Like most of the segments Volex operates in the EV power cord market is highly fragmented with many smaller local players where Volex is one of the few large international businesses that design, test and build EV power cords.

There are two broad categories of EV power cords, DC power cords and AC power cords. Virtually all of the power in our power grid is AC and an EV needs DC power. The difference between DC power cords and AC power cords is where the conversion from AC to DC happens. In AC power cords the conversion happens in the car and therefore charging is slower. DC cords are attached to a station that coverts the power and therefore can charge the car substantially quicker. Because the DC cords need a power station they are almost exclusively found out of the home in public infrastructure and it is DC cords that are likely to replace highway gas stations where speed of charging is important. On the other hand, AC power cords are used for charging in the home and at the office where speed is not the priority. Currently the vast majority of EV charging is AC power cords.

Volex was one of the first major global player in the AC power cord market and is still currently one of the only global suppliers of grid cords. Volex supplies power cords to the biggest EV manufacturers, either directly like they do with Tesla – where Volex is the sole-source supplier - or indirectly via tier 1 suppliers like Aptiv. Moreover, Volex is the partner of choice in the industry as it is not only the low-cost producer, it also has a brand synonymous with quality and reliability. Volex is building its expertise in EV charging solutions, expanding its offering from purely AC power cords to recently manufacturing the charging head, further expanding its ability to control quality and lower prices. Industry trends show large future growth in public DC charging stations as governments invest in infrastructure for the new electric world. Volex has responded to this trend by investing in DC power solutions and has recently started manufacturing its own DC charging products. Industry projections show that AC charging will continue to dominate the market with the bulk of charging happening at home or at the office.

The EV power cord market is still in its infancy and has a long runway of extremely high growth rate in front of it. The EV power cord market will grow as EVs start to become a larger part of light domestic vehicle (LDV) sales. Currently EVs – which includes plug-in hybrids - make up less than 10% of global LDV sales. However, many countries have policies in place encouraging consumers to switch to EVs and many countries have announced bans on fossil fuel cars such as all 27 EU countries by 2035, Norway by 2025, the UK by 2030 and a number of provinces in China by 2030. With the current announced pledges EVs are likely to make up at least 50% of LDV sales by 2030, and if the world wants to hit its net zero 2050 goals EVs will need to make up close to 70% of all LDV sales. In the US, the EV charging cord market is expected to grow at above 30% CAGR for the next 5 years, reaching a total addressable market in the US of $2.5billion, the global market is expected to grow at a faster pace reaching a total market size of $180billion by 2030.

Outside of the light vehicle space there is opportunities for Volex to capture the growth of other types of electric vehicles such as two wheelers – mainly e-bikes- over 95% of which are in China and have yet to be adopted at scale in other countries. China has already begun to electrify its bus and taxi fleets, over 90% of electric buses are in China. In accordance with already announced pledges the number of bus depot chargers is going to more than 10x in the next 7 years going from 65,000 today to over 750,000 in 2030. Moreover, growth in electric truck depot chargers is to experience parabolic growth – albeit off a tiny base - going from 7,000 today to over 390,000 in 2030. As the world starts to electrify its buses, taxis and heavy vehicles consumers will need more complicated and powerful charging solutions from a large-scale manufacturer. Arguably it is only Volex who is currently well positioned to take full advantage of this transition in the EV power cord market.

In the EV power cord market there are barriers to entry such as a myriad of health and safety regulations across many jurisdictions and the technical expertise to deliver the high quality, waterproof and durable cords demanded by customers. Alongside being the low-cost producer this gives Volex a considerable moat to earn economic profits for the foreseeable future.

We expect that Volex’s EV segment will grow at the same rate as the overall EV charging cord market, we expect that more competition will enter the market as the total addressable market grows and although Volex is likely to be able to defend its position as market leader due to its first mover, scale, low cost and brand advantages, it is likely to have lower overall market share. However, we also do expect Volex to broaden its offering in the segment, we have already seen with them starting to expand into manufacturing charging heads and DC charging cords.

Complex industrial Technology

The Complex Industrial Technology segment is a broad segment that covers many industries, some of which we could see becoming their own segments in the near future. Currently this segment covers Defence and Aerospace, Data Centre, Industrial and Off-Highway transport. We will briefly cover some of these markets however, we think that the Data Centre market is the market that holds the most opportunity for Volex, and therefore, our focus will be on the Data Centre market.

Volex has been a leading, fully integrated, manufacturer of high-speed copper cables since 2007. Volex has unrivalled market leading expertise in high-speed copper cables and have in the past been approached by big multi-national retailers to design and manufacture high-speed copper cables with requirements that other suppliers simply couldn’t meet. High-speed copper cables are used in data centres to transfer data at extremely high rates, Volex have designed high-speed copper cables capable of delivering data rates of 800Gbps. Data centres need copper cables to transfer data over a short range usually where the cable needs to be bent. This is the key advantage over fibre-glass, as fibre-glass is great at transporting data over long distances in a straight line but it is inflexible and can’t be bent. Typically, short (less than 3m) high-speed copper cables are used to transfer data within the data centre and fibre-glass is used to transmit data out of the data centre. Alongside high-speed copper cables Volex designs and manufactures data centre power cords that deliver power to specialised computers and servers. This can range from Volex’s off-the-shelf power cords, which are cheap and low margin, to custom engineered power solutions that includes specialised cords and servicing expertise, which commands higher margins.

Throughout the data centre value chain there are highly fragmented markets, for suppliers of power systems and high-speed copper cables there are very few global players and the market is characterised by many small local manufacturers. The owners of data centres are characterised by a highly fragmented market of big international customers such as Amazon, Google, Apple, Cisco, IBM and many more. This leaves Volex as one of the few large-scale global suppliers in a very favourable position where they have a diverse customer base of large international blue-chip companies while it competes against smaller competitors that can’t offer large scale global supply. The market also offers a long runway for Volex to acquire competitors at low multiples and integrate them into Volex and apply best practices.

The move towards cloud; companies increasingly focusing on data analytics and the continuing expansion of IoT services are just a few of the structural tailwinds that will help sustain high rates of growth in data centres. A 2020 Domo report estimated that 1.7mb of data was created every second for every person on earth - that is a lot of data that needs to be stored somewhere. Depending on how it is defined the global data centre market is estimated to be about of $215 billion – the data centre power market makes up about $8billion of this total - with experts producing wide ranging estimates of growth from 9%-26% CAGR till 2030. The US data centre market is the biggest by a considerable margin and is likely to remain the biggest for a long time to come. This is a huge advantage for Volex which has a global manufacturing footprint as it can offer data centre solutions tariff-free and makes competition from China unviable.

The trend in the industry is that international data centre owners are expanding into Hyperscale data centres where data is stored in a low number of huge, highly complex, data centres. This means that data centre owners are looking for suppliers that are capable of manufacturing at scale and that have expertise in highly complex designs. Volex is positioning its self to be the one-stop-supplier of power and high-speed copper cable solutions for Hyperscale data centres, working with customers from the design stage and using their expertise to engineer custom solutions.

Data centres go through roughly 18-month upgrade cycles and look to partners that they can trust over the long term. Therefore, data centre revenues are generally recurring and sticky. Volex is well positioned to be the trusted partner and the low-cost producer in the industry. These 18-month cycles can make revenues lumpy and unattractive for new entrants. There is currently a large upgrade cycle underway to the new 400Gps cable - in which Volex was the first mover -, and this should show up in 2023 sales. Due to this upgrade cycle Volex’s data centre sales were very soft in 2022, with the Complex Industrial Technology segment growing at 12% excluding data centres, instead of the stated 6%. This has also led Volex to increase their inventories to prepare for the big growth in data centre sales next year, which partially explains the increase in debt and the lower cash conversion Volex experienced in 2022.

Volex provides integrated manufacturing services to markets such as Defence & Aerospace, Industrial and Off-Highway Transport, supporting clients from concept to reality. Volex is a top-tier supplier of high-value add, high margin, products such as printed circuit boards, box builds, electrical harnesses and highly engineered custom power solutions. All of the products Volex makes in these markets are specialised and are highly regulated where Volex is the trusted partner with the highest safety accreditations. Volex has been very selective about the markets it has entered, choosing only to enter markets where it has a clear competitive advantage. We have seen Volex recently acquire two new top-tier Defence & Aerospace suppliers that has given Volex access to blue-chip customers such as Boeing. We expect that in the near future Defence & Aerospace will be its own segment as we see Volex investing and growing in the area. Like the other markets Volex operates in Defence & Aerospace is a highly fragmented market with a long runway of acquisitions and organic growth ahead. In the Industrial market the transition to factory automation and smart infrastructure is proving structural tailwinds and the market is likely to see sustained high growth rates. We have also seen competitors expand their industrial offerings into robotics and sensors which are potential new markets for Volex. We have seen Volex acquire a manufacture of box builds and printed circuit boards in India along with a large plot of land for factory expansion. As Volex invests in the Industrial market we are likely to see it play a bigger role in Volex’s sales mix and eventually could become its own segment.

MEDICAL

Volex is a global leader in integrated manufacturing and support services for medical devices. Volex works with medical device manufactures such as Philips on designing power solutions, then tests, builds and services these medical device power solutions – everything from low margin hospital grade power cords and printed circuit boards to high margin complete system integration and complex box builds. Medical device manufactures want a long-term partner because once a device has regulatory approval it cannot be modified without having to go through the laborious process of getting it reapproved. Typically, a medical device will be in production for about 5-10 years before it becomes obsolete, this varying depending on the technology some machines can be upwards of 20 years. First, this means recurring and sticky revenues for chosen partners. Secondly it is critical to the big medical device companies that their suppliers will still be around over the life of a device. On multiple occasions big medical device companies have approached Volex asking Volex to acquire a certain supplier because that supplier perhaps has some specialist expertise that the medical device manufacturer needs but is too small to currently produce that part on scale or there is something going on at a current supplier that is making the medical device manufacturer nervous and would be grateful to Volex in giving that business a stable home – for example the supplier has built up too much debt, the CEO retiring or the current owners is not reinvesting in the business. When this has happened in the past Volex has been able to acquire fantastic business with blue-chip customers, for a very low valuation, while the medical device manufacturer guarantees Volex continued business.

The medical device industry is heavily regulated with products having to go through rigorous testing to achieve the correct certifications. The big medical device companies rarely accept suppliers with just the basic certifications they require extra certificates that are often backed by the big medical manufacturers themselves. This provides very high barriers to entry especially for manufacturers in low wage countries such as China. Volex is one of the few companies that have a global footprint of factories in low wage countries – Mexico, Slovakia and Indonesia – with the highest levels of certifications. In 2022, Volex Tijuana became the first Mexican manufacturer to receive the highly coveted MedAccred Accreditation which is subscribed by Bausch Health, J&J, Philips, Roche and many other big medical device manufacturers. This is a huge success for Volex as it puts them in the unique position of having near-shore, tariff-free, access to the American market with the highest Health & Safety accreditation while also having access to low cost manufacturing.

In addition to having the highest health & safety standards Volex is the “trusted-partner” for global medical device manufacturers who need a supplier that meets their global needs and Volex is the low-cost producer in the industry having highly automated factories in low cost countries. The industry is fragmented with many small specialist suppliers, this is a great set-up for Volex’s acquisition driven business model with a lot of space for Volex to grow both organically and inorganically. The medical device industry is relatively mature and is predicted to grow at a roughly 6% CAGR till 2030, driven by: an increased focus on health; an aging population and a trend towards wearable medical devices. Volex is likely to see a temporary boost in 2023 as elective surgeries continue to recover from the pandemic which stopped people getting elective surgeries. Volex is likely to organically grow at about market rates as it is benefiting from the trend of near-shoring where American and European manufactures are looking for trusted partners closer to their end markets. Volex has slowed its investments in China to focus on expanding globally, Volex is uniquely positioned to benefit from near shoring.

Volex’s Consumer Electronics sales Consumer electronics

Consumer Electronics used to make up over two-thirds of Volex’s sales. Today that is down to 43% of sales. Volex has consistently been one of the top 3 global players in AC power cords, and after recent acquisitions it has cemented its positon at the top. The Consumer Electronics market is highly competitive with products having very little differentiation, think of a 2m power cord found on a kettle or TV. Gross margins across the industry are typically below 15% and very few companies make an economic profit. The industry in concentrated in China and Japan due to the access to cheap and highly efficient manufacturing. Tariffs forced upon China by the Trump administration have shocked the cost sensitive industry, without tariff-free access to cheap Chinese manufacturing customers have been looking for cheap manufacturing closer to end-markets. Volex being a truly global manufacture has been expanding into markets just and Indonesia, Turkey and Mexico to offer global tariff-free supply.

In 2021 Volex made the truly transformational acquisition of DE-KA, which is likely the most efficient and lowest cost producer of AC power cords in the industry. DE-KA have highly automated factories in Romania and Turkey, that produce high volume, low mix products, potentially having less than 20 high volume SKUs like 3m black power cords. Despite selling undifferentiated products DE-KA is so efficient it has consistently had 14% net profit margins, whereas most competitors barely achieve 14% gross margins. With the acquisition of DE-KA and the highly efficient factories Volex has in Mexico and Indonesia, Volex is able to offer the lowest cost cords, tariff-free, across America, Europe and Asia. Whereas previously a consumer electronics manufactures may have used Volex’s cords in Asia but not Europe, now Volex can cross-sell and be the global supplier of AC power cords to global manufacturers.

Alongside being the low-cost producer, Volex is transforming the business to compete in areas where the customer has a reputation to protect and is willing to pay slightly more for quality, for example Dyson and Sony.

The Consumer Electrics industry is highly fragmented with many small players centred in China and Japan. Volex is in a fantastic position to provide a home for highly efficient businesses like DE-KA and expand its global offering. We also expect Volex to continue to vertically integrate, acquiring more of its own copper and plastic supply to reduce the cost of its products and widen its moat as the low-cost producer. Finally, the Consumer Electronics market is mature and unlikely to grow much above 5%, with potential upside if the work-from-home trend stays, which will lead to greater demand. The 60% growth in 2022 was due to this being the first full year of having DE-KA as part of the business and factory expansion. Volex should be able to grow organically slightly above market trend as it benefits from near-shoring, cross-selling and factory expansion.

Management

We believe that Volex has the best management in the industry by a considerable margin and the success that they have already shown gives us confidence to say that management are great capital allocators with a long runway ahead of them.

CEO Nathanial Rothschild is the largest shareholder of Volex, with roughly 25% ownership through his investment vehicle NR Holdings Limited. Rothschild is a British financier and investor who is also the heir apparent to the “Baron Rothschild” title and fortune. Having been in the public eye as a rebellious youngster Rothschild has completely changed course and seems to be dedicated to hard work and protecting the family legacy. He has served on the boards of various public companies and has a wealth of experience in investing such as being co-chairman of Atticus Capital. We think that Rothschild’s deep business and political connections are a huge benefit to Volex as he is able to utilize his network to bring in extremely high calibre people into Volex and open doors to financing and deals usually shut to a company the size of Volex. We think that Rothschild’s influence can be seen in Volex’s highly qualified board that includes the likes of an incredibly distinguished British diplomat who will no doubt help Volex navigate its ever-growing international presence.

We believe that during the almost 7 years Rothschild has been the CEO and Chairman of Volex, he has proven himself to be truly excellent capital allocator and has completely transformed the business. Not only has he set very ambitious goals for himself in the past but he has blown past those goals, achieving his lofty 2024 revenue and profit goals in 2022. Rothschild puts emphasis on being aligned with shareholder, not only does he show this through his 25% ownership of the business, but also the fact he has a very reasonable salary with a bonus tied to 50% long-term total shareholder return and 50% long-term cumulative operating profit. He has created a very open dialog with shareholders and truly treats shareholders like partners.

We think Rothschild has a true “outsider” mind-set, he has already cut headcount at head office by 40% and has decentralised operations choosing to partner with exceptional management that have a lot of autonomy. Moreover, he is implementing a culture of owner-mind-set where local management have a stake in Volex and run their operation as if it was their own, with the businesses being driven by a Kaizen approach. Rothschild is a big believer in the Kaizen approach, which is the Japanese business approach of continual improvement and ever-increasing efficiency. He has successfully implement the Kaizen approach at Volex where they have been continually improving factory efficiency and automation, trying to make their position as the low-cost producer unassailable. We think that Rothschild’s past success is just the start of what he plans to do at Volex, he again has set very ambitious goals to double the size of the business over the next 5 years. However, we think the fact he has placed Volex in high growth markets like EVs and data centres he will be able to blow past these expectations yet again. When Rothschild first took the helm, he focused on getting the existing businesses in order, however in the last two years we have seen a greater focus on acquisitions which look to be extremely value creating and low risk.

Capital allocation

Rothschild has shown a focus on diligent capital allocations and only choosing projects with high IRRs. Most of the growth capital expenditures he has implemented during his time have had a 2-year payback. The capital expenditures have consisted of factory expansions, factory automations and expanding its vertical integration. We believe Volex has a long runway of internal high return investments and we expect to see capital expenditure climb from 2.4% of revenue in 2022, to 4% - 5% of revenue depending on the opportunities. This will be driven primarily by Volex’s expansion in fast growing markets such as EV and data centre. Volex has already committed to large factory expansions over the next 18months – India 250% expansion, Indonesia 52%, Poland 75%, and Mexico 22%. As well as a large set of internal high return opportunities, Volex has set about acquiring extremely high-quality businesses with excellent management for very low valuations.

Rothschild has been transforming Volex into the home for excellent businesses where management are treated like partners with high levels of autonomy. This has already paid off massive dividends for Volex, DE-KA being the most efficient and profitable player in AC power cords market had very little reason to want to be acquired. DE-KA’s management were not interested in selling as management seen the business as their own and wanted to keep it that way. However, Volex offered DE-KA a home where management could have “skin in the game” and still run it like it was their own. Volex ended up getting the best in class business with eight-year revenue and EBITDA CAGR of 9% and 28% respectively, for a mere 6.9x EBITDA multiple. After considering the massive growth potential of DE-KA, post-integration synergies and cross-selling opportunities this acquisition seems even cheaper.

Since Rothschild became CEO Volex has made a total of 10 acquisitions at an average acquisition price of 5.5x EBITDA. Rothschild has shown a discipline for waiting to find high quality businesses with great management, which he understands very well and that can be acquired at an extremely cheap valuation. Moreover, as we previously mentioned acquisition targets have been suggested by large OEMs who guarantee Volex sales if they acquire the target, this is creating win-win-win situations, where the OEM is winning because they get a stable global supplier, the takeover target is winning because they get paid and are still able to run the business as if it was their own and finally Volex is winning because they get a well-managed business for a very low price with guaranteed blue-chip customers. Furthermore, once acquired Volex set about applying best practices, investing and growing these business and cross-selling. Newly acquired businesses will give Volex an ever-growing pipeline of high return internal investments where they can apply what has worked in the past to these new businesses. So far, this acquisition strategy has been immensely value creating and we believe that there is a huge opportunity set out there for Volex as they operate in massive markets that are highly fragmented, we believe that this acquisition strategy could easily last decades without running into problems.

risks

Competition

Volex operates in highly competitive markets often with little or no product differentiation. Volex’s solution to this is to be the low-cost producer, with the best reputation for quality and have the biggest scale. It’s a tall order for operating margins that are unlikely to exceed 10%. However, we think that Volex is well positioned to achieve this goal and once they do it will be very hard to displace them with very little incentive for new entrants. Volex have shown their intention of being long-term greedy by keeping margins low and we hope this will continue in the future, a threat to this strategy is that Volex start using their scale to charge higher prices and gouge customers, this will not end well. The only way to be truly successful in this industry is to have win-win propositions and be the low-cost producer.

Volex’s shift towards higher margin products has not gone unnoticed, our competition analysis has shown many competitors starting to shift towards different niche businesses and exiting low margin businesses. The competition is at different stages of transforming their businesses with Volex’s closest competitor TT Electronics having successfully transformed its business towards specialising in Healthcare, Aerospace & Defence and Automation, with TT Electronics current margins at 8% and goals of getting them above 10%. TT Electronics, like Volex, has started to focus on M&A and aggressive internal investments, with TT Electronics targeting 5% of revenues going towards R&D. TT Electronics has also diversified away from Power Solutions expanding into sensing capabilities. Another major competitor that is trying to follow in Volex’s footsteps is Leoni. Leoni is far bigger than Volex doing 5 billion Euros in sales in 2021 with a specialisation in the automotive industry (which makes up about 84% of their sales). Leoni is still currently an extremely low margin and unprofitable businesses that is just starting on their restructuring journey by selling off large business units. We think that respectable competitors like TT Electronics could provide competition for acquisitions in the future. Therefore, it is important that Volex cements its reputation as the best home for businesses with entrepreneurs who wish to continue running their business. Volex has arguably the best position in the industries it operates in where it is the low-cost producer, most trust brand and largest scale producer – this gives Volex an incredible moat. Volex’s biggest differentiator when it comes to growth and acquisitions is Volex’s management, culture and capital allocation, we think it is unrivalled in the industry.

Management

We have made it clear that a big reason we like Volex is the management and these are the sort of people we want to partner with for the long-term. However, despite Rothschild still being relatively young, 51years old, there is no guarantee how long he will stay at Volex. Although there are benefits to having an independently wealthy and experienced global tycoon at the helm of Volex, it could also have its downsides. Being heir apparent to the “Baron Rothschild” title and fortune comes with publicity and perhaps responsibilities that might force him to step away from Volex. Rothschild is both CEO and Chairman of the board which gives him a lot of power over where Volex goes. For the most part, we like that Rothschild has this freedom to act as an owner and he doesn’t take any extra salary for as the Chairman of the board. However, given that some sources put his net worth in excess of $40billion it is foreseeable that during a period of weak share price, Rothschild could take Volex private, and leave long-term shareholders like ourselves disappointed. However, we believe Rothschild respects Volex’s shareholders and have our best interests in mind. Moreover, if he was to leave, we believe that he would carefully put in place a multi-year succession plan, like he did when CFO Darren Morris stepped down to be replaced by Jon Boaden who had shadowed Morris as Deputy CFO for the better part of two years.

Customer concentration

Despite having diversified their customer base Volex still have two large customers which combined account for 27.6% of revenues. One customer is in the Medical sector which we infer to be Philips and the other in the EV sector which we infer to be Tesla. Unlike in the past where Volex was beholden to Apple this time Volex is suppling high value add products to these two customers and Volex has bargaining power. Moreover, Volex’s customer base is far more diversified than it was in 2014 when it was reliant on Apple and we expect Volex to continue to diversify its customer base. It is natural that Tesla is such a big customer for Volex as Volex is Tesla’s sole-supplier of AC power cords, as we see more entrants and competition in the EV space we expect that Volex will naturally diversify its sales away from Tesla in the EV segment and won’t have the same problems it did with Apple.

Inflation

Volex uses a lot of copper in its products and, despite starting to vertically integrate, Volex still is a big buyer of copper. However, it is the industry standard that copper and transport costs are passed through to the end customer. There is a slight lag in passing through the prices, Volex attributes a 1.3% margin compression in 2022 to inflation and for the most part has been able to quickly pass through inflation as copper prices soared. Volex is quite insulated from inflation and can pass on its costs easily. However, big spikes in copper may not directly affect Volex’s margin but it may reduce consumer demand and consumers may look for alternatives to copper wiring. We are currently seeing copper prices fall from the extreme highs of 2021 and we don’t expect copper prices to destroy consumer in the near future.

Wireless charging

Inductive charging known as Wireless charging is posing a threat to the cord market and in theory wireless charging could eliminate the need for cords, especially in the EV market where wireless charging equipment could be place under roads and parking lots. However, so far all wireless chargers still need to be plugged in with a cord and the technology does not seem to currently be applicable in the EV market. For now we don’t see wireless charging as a threat to Volex, however, we will continue to monitor the developments to see if it may pose a threat to power cords in the future.

Valuation

In valuating Volex we only try to value the business as it is today, we cannot value positive acquisitions that have not happened. Therefore, this valuation is purely organic growth from aggressive high return capital expenditure. The likelihood of further value creating acquisitions gives us a greater margin of safety than what the numbers state.

We have separated out each segment for revenues and then assume that the overall operating margins are 10%. We separated out the segments not for the added, false, sense of precision but to explicitly state our assumption and then to be able to update and learn from those assumptions when we are inevitably wrong. Despite the high margin segments such as Complex Industrial Technologies and EV being a larger part of the revenue mix we assume that Volex uses this extra margin to build its competitive moat by either training employees or lowering prices.

Throughout this valuation we think we have been very conservative. We have not given any value to the current $64.1 million of unrealised tax losses for which we think Volex will eventually be able to recognise as a deferred tax asset. Furthermore, we assume Volex pays the British corporate tax rate of 19% however, historically they have payed less than 19%. In 2021 Volex had an effective tax rate of -17% (due to the recognition of tax losses) and 2020 11.4%.

We also assume that Volex continues to have debt in the business and that they incur financial chargers over our valuation. For most of the time Rothschild has been CEO Volex has been debt free however, we do believe going forward that having debt as part of the capital structure makes sense and gives management more fire power for investment.

Throughout all of our scenarios we expect management to ramp up capital expenditures to fund growth, doubling from the current level of 2.4% of revenues to about 5% of revenues. This makes free cash-flow optically low on our valuations and maintenance capital expenditure is far below the figures.

We believe that as Volex grows they will have to increase their networking capital in the businesses and we conservatory account for that in our valuations.

Despite the company focusing on EBITDA we have used a free cash multiple as we think this is suitable for this type of business. In this commentary we have provided an EBITDA multiple for comparison but we don’t find it very instructive.

In our Bear case we assume that management increase capital expenditure to about 5% of revenues however don’t create substantial growth. Moreover, we assume that the large factory expansions that Volex have planned don’t lead to substantial growth. Moreover, we assume that all of Volex’s segments grow below industry expectations leading to loss of market share. We still assume that management can keep margins in their 9%-10% range but in our Bear case we assume that they can only reach a 9% margin. Finally, we put a 12x multiple on depressed free cash flows (5x EBITDA) as a very conservative multiple and at the very low end of the industry spectrum.

In our base case we assume that there is a boost to the Complex Industrial Technology segment from the cyclical upgrade of data cables. We also assume that the EV segment grows below market expectations but still at a reasonable rate. We don’t assume that Consumer Electronics segment will see much growth despite the planned expansions of DE-KA facilities. For the other two segments we merely assume market growth rates. For our base case we assume an average P/FCF multiple of 15x (7.1x EBITDA).

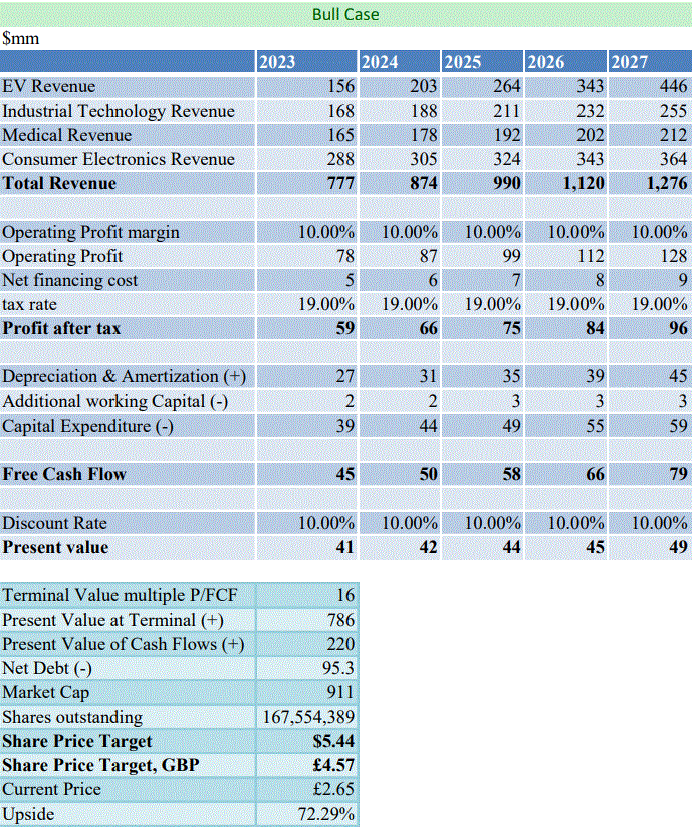

Finally in our Bull case we assume that Volex gains market share in all segments growing slightly above market rates. We also assume that factory expansions and the data centre upgrade cycle lead to an increase in sales. We assume a slightly above average terminal multiple of 16x P/FCF due to the scale and quality of the business. We feel that if the market was to recognize the quality of Volex and the immense talent of its management we think it could trade at a much higher multiple like its serial-acquirer peers for example another British serial-acquirer Judges Scientific often trades at P/FCF multiples well above 20. However, due to the commodity nature of Volex we are comfortable with a conservative 16x P/FCF multiple.

We believe that while Rothschild’s goal to break a billion in sales seems ambitious on the face of it, when you take into account the amount of expansions Volex is doing and the fast growing markets Volex is in we believe he will be able to achieve these goals organically through investing in the current business. We also feel comfortable saying that over the next five years Rothschild and his team will do more value creating acquisitions which we don’t include in our valuations giving us a bigger margin of safety than the numbers suggest.

Conclusion

In our opinion Volex has a uniquely strong moat in an otherwise fractured and commoditized market. We think management have extraordinary capital allocation skills and they are the type of people we want to partner with. The unique decentralised culture of owner-mind-set and Kaizen that Rothschild has instilled throughout Volex will continue to be a hard to replicate moat that will drive the business forward. Moreover, Rothschild has positioned Volex in relatively high-margin and high growth industries where there is a long runway for astute capital allocators, to grow both organically and inorganically. We have seen 10 value creating acquisitions and we expect to see a lot more in the future. Volex has been a multi-bagger since Rothschild took over, and we see accelerated growth and a long runway of acquisitions ahead of Volex and expect it to be multi-bagger from here. Currently we feel that the market is offering investors a chance to partner with incredible capital allocators with a substantial margin of safety in the price.

White Loch Capital Management is a fictitious fund used for educational purposes only

Thanks for reading

Email: whitelochcapitalmanagement@gmail.com

Twitter: @WhiteLochCM

Disclaimer: Do not interpret anything above as financial advice. This article has been prepared for informational & educational purposes only. The writing contains certain forward-looking statements and opinions which are based on the Author’s analysis of publicly available information believed to be accurate and reliable. While the Author believes that such forward-looking statements and opinions are reasonable, they are subject to unknown risks, uncertainties and other factors that could cause actual results to differ materially from those projected. As of the date the Report is published, the Author may or may not hold a position in the security mentioned. Nothing in this Report constitutes investment advice. Readers should conduct their own due diligence and research and make their own investment decisions. This is NOT a buy or sell recommendation.