a2 Milk (ASX: $A2M) (NZX: $ATM)

A top FMCG brand with a long runway of growth ahead being offered at a massive discount, base case 100%+ upside

Highlights

· Over 100% upside from base case

· Compounder with a long runway for growth

· A top FMCG brand

· Extremely high margin business

· Massive cash position on balance sheet

· A confluence of macro tailwinds at its back

· Capital light business with high ROIC

Graphs and images can be found in the PDF version of this article.

Disclaimer: White Loch Capital Management is a fictions fund that is used purely for educational purposes. The author uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. You are advised to discuss your investment options with your financial advisers, including whether any investment is suitable for your specific needs. Following publication, the Author may transact in the securities mentioned. All expressions of opinion are subject to change without notice, and the author does not undertake to update this report or any information herein.

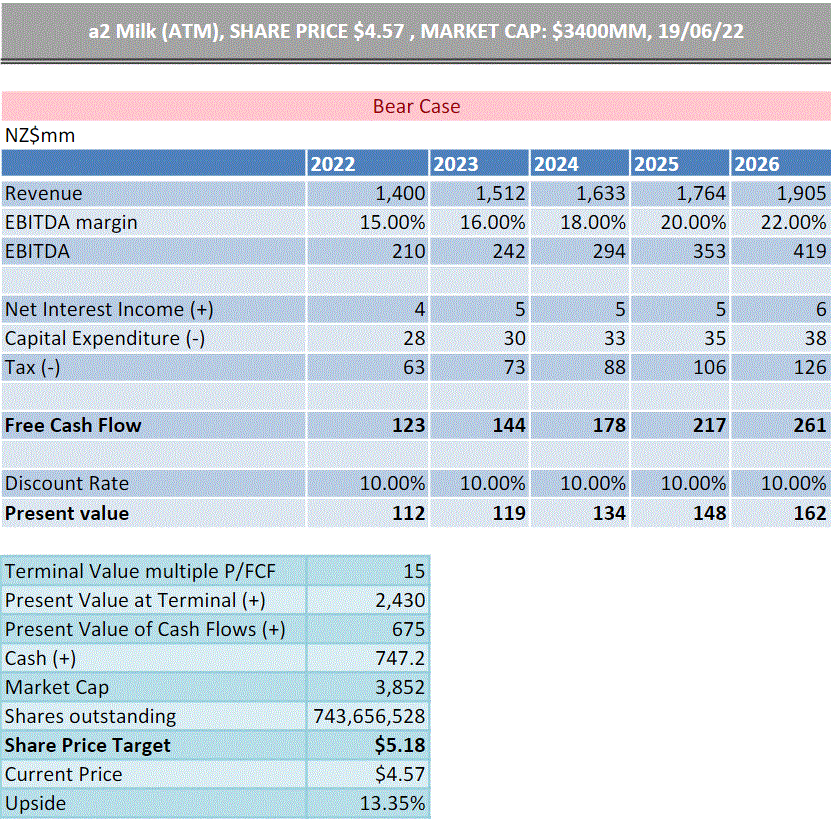

a2 Milk (ATM), SHARE PRICE $4.57 , MARKET CAP: $3400MM, 19/06/22

Executive summary

White Loch Capital Management believes that the market is offering investors a top FMCG brand at bargain price, conservatively offering more than a 100% upside in our base case. The a2 Milk Company (A2M) is a capital light brand with a long road of compounding ahead of it. However, the business was badly hurt by the effects of Covid, with EBITDA plunging over 70%. The market is pricing in that this great compounder won’t recover and is destined to turn into a capital intense low margin dairy company. Furthermore, we believe the market perceives A2M’s competitive advantage as a scientific or patent protected one where new entrants could come in with similar products. However, we think A2M’s competitive advantage is the incredibly strong brand it has built with Chinese consumers trusting A2M to provide nutrition to their families. Finally, in 2021 new management was put in place and signs of a turnaround can already be seen. New management are coming into the business at the perfect time, huge draw down in share price, revenues and margins have been hit badly and the company is sitting on a horde of cash, roughly 22% of market cap, which give this new management a lot of fire power. We think that it will hard for management not to look like a huge turnaround success.

The business

he a2 Milk Company (A2M) was founded in New Zealand in 2000, by Dr McLachlan who was a scientist studying the effects of A1 beta-casein and Mr Paterson, a wealthy New Zealander with experience in the dairy industry. A2M claimed that studies showed that A1 proteins found in milk could be harmful to drinkers and that A1-free milk (a2 milk) had health benefits, higher protein content and was easier to digest, including for drinkers with lactose intolerance. A2M went on to commercialise genetic tests to determine whether a cow will produce milk without the A1 protein. The path has not always been straight forward for A2M with both founders dying and a series of fierce litigation battles early in the life of the business. However, from the ashes arose a capital light brand that has been widely adopted by consumers in China and Australia.

China was the perfect market for A2M to enter, it has extremely high lactose intolerance rates and A2M claims to have a product that gives lactose intolerant drinkers less discomfort and is easier to digest –de Vrese M, et al. 2001, found that above 90% of all adults in East Asia are lactose intolerant. Moreover, when A2M launched their products into China it was in the wake of the 2008 melamine scandal which had injured over 300,000 Chinese babies and killed at least 6. Chinese mothers were eschewing local brands and were screaming out for foreign brands that they could trust.

A2M was the first mover in the a2 milk space and created the category single handily. A2M has experienced hyperbolic growth since inception, Going from a science, concept, based business in 2000 with only $7mm in sales into a status-brand, multi-category nutrition leader with over $1.73bn in 2020. Initially they had a technological and first mover advantage, however that advantage has now eroded and there are many new entrants coming into the fast growing a2 milk market.

We don’t think of A2M as just another dairy company that had a patent protected product, and that now their product will be commoditized. We think the right way to think about A2M is an asset-light, incredibly strong FMCG brand. A2M has very little capital in the business and have partnerships along the value chain – akin to the Coke - coke bottler relationship. Its products have been affectionately termed the "Hermes of milk" by affluent Chinese consumers willing to pay massive mark-ups. The way we see A2M developing is as a luxury brand, which consumers trust throughout their lifecycle – trusting the brand to feed their babies, provide their families with the highest quality dairy products and offer nutritional support later in life.

Infant Nutrition

Infant nutrition is by far the biggest segment for A2M, in 2021 A2M did $913mm in infant nutrition sales accounting for over 75% of total sales and the vast majority of the profit. A2M run a two label strategy – an English label and a Chinese label. The bulk of both the English label and the Chinese label ends up being consumed in China with a number of different routes to market, some of which are complicated and opaque.

A2M place its infant nutrition products in the “Ultra-Premium” category, with a strong focus on building a brand and growing consumer awareness. A2M has about a 5% market share of the Chinese infant milk formula (IMF) market, its products generally command the biggest price premium. Being a dominant player in the ultra-premium space A2M has grown and will continue to grow alongside the Chinese middle and upper class. This has had a large effect on where A2M’s customers are located in China, with A2M having a disproportionate amount of their customers residing in Key&A cities like Beijing and Shanghai, while in the lower tier cities families are generally less wealthy and often have to settle for cheaper local brands.

Although overall market share is only 5%, A2M’s market share varies drastically depending on the route to market with much higher market share in the fast growing digital route to market. This is congruent with the rise of China’s young middle class who have different shopping habits than the generations before them, with A2M being extremely well positioned to take advantage of these trends.

A2M have an understanding that above all when a mother is choosing what to feed her child that brand trust is the most important consideration. This is even truer in China after the terrible 2008 scandal which has left Chinese consumers suspicious of local brands and principally valuing trust. A2M’s brand is arguably the strongest in the market and punches well above its weight on brand metrics. In 2021 A2M commanded both the highest and second highest Net Promotor score in the Chinese IMF category and had close to 50% brand awareness.

A2M have focused on their “one brand, two labels” strategy which gives consumers the choice between a Chinese label and an English label. The China label is the higher priced of the two with added nutritional benefits such as lactoferrin. The English label sits at a slightly less lofty price and is more accessible to lower income families. Despite the China label being priced at a premium it actually delivers lower margins as distribution and other costs are higher. In the past the English label has dominated A2M’s infant nutrition sales however the China label has been growing at a much faster rate and in 2021 made up about 39% of total infant nutrition sales. The biggest difference between the two labels is their route to market.

China Label

n 2021 the China Label segment did $389.9mm in sales, seeing a 15.4%YoY increase in sales as Covid lockdowns spurred consumers to pantry stock and consumers were finding it more difficult to get a hold of the English Label as these channels were far more affected by Covid lockdowns. Although the China Label channels were less affected A2M made the tough decision to write down $50.3mm worth of China Label inventories. Since the introduction of the China label in 2016 growth has been tremendous, growing from 2016 $4.9mm in sales to 2021 $389.9mm, 107% CAGR.

There are three main China label channels: Mother and Baby Stores (MBS); Modern Trade (MT), includes supermarkets and convenience stores; Domestic Online (DOL). We think going forward the China Label channels will continue to grow and become an ever larger part of A2M’s sales. Despite China Label having lower margins than the English label, the margins in the China & Other Segment are still very high, with 2019 EBITDA margins around 32%. However, margins tumbled to 13% in 2021 due to inventory write-downs and channel mix. We also think the growth in the China Label segment marks a great opportunity for A2M as these channels are much more transparent and the business has greater control over its branding and products.

MBS is an extremely important channel for A2M not only because of 22.8K stores that they distribute to but this channel serves as a key platform for doing in person brand building and marketing events. MBS is critical for getting access directly to mothers and we have seen A2M huge host events in this category despite only having a 2.5% market share in the MBS market. Though 2.5% market share might seem unimpressive A2M has increased its market share from only 2% in 2020 and was one of the few foreign brands to increase market share. A2M believes the MBS channel is where the company’s best opportunities are to gain market share and have made it a key priority in its new growth strategy, with goals of being in 35K stores with a 5% market share.

The MBS category has been, and will continue to be, driven by growth from lower tier cities where A2M has a relatively lower market share. This poses a challenge to A2M as growth is going to come from markets where they typically haven’t done as well. However it also offers great opportunities as the lower tier cities are growing, becoming wealthier and will see a rise in their own young middle and upper class that aspire to consume the same brands as their top tier city peers. We think, MBS is a relatively difficult environment to compete in because these stores tend to hold a wide selection of brands many of whom are also doing marketing events, compared to MT where many stores only offer a handful of brands.

The MT channel currently serves mainly for distributing non-IMF products like fresh milk. However, we think that there could potentially be a big opportunity in this channel. Over the past 5 years we have seen a very profound change in shopping habits in Shanghai, moving away from local open air markets to supermarkets, in particularly the rise of HeMa, the Alibaba retail arm and premium-supermarkets like Olé. HeMa has revolutionised grocery shopping for many residents in top tier cities. HeMa has the scale and selection range comparable to supermarkets found in Europe, with the main method of payment the HeMa app at a self-checkout or using the HeMa app to shop remotely and get it delivered to your door. The rise of supermarkets in China has been a recent one, something we have witnessed over the last five years. The move towards supermarkets has been dramatically sped up by the pandemic, with many of the open air markets now shut down in Beijing and Shanghai. This is important for A2M because open air markets did not have infant formula and Chinese consumers were buying their groceries and infant formula in different places. However, with the rise of supermarkets like HeMa consumers can buy their IMF while they grocery shop. There are usually only a handful of IMF brands available in the supermarket, with A2M being by far the most ubiquitous from our findings in Shanghai. We have yet to see a HeMa in Shanghai that didn’t fully stock all of A2M’s IMF range. Moreover, during the most recent lockdown in Shanghai –April 2022 – June 2022 -, many households were trapped with no way to get food other than a HeMa delivery or a community group buy. Checking the HeMa app daily we found that the majority of the time during this period the only IMF available to buy was A2M’s products. This is all anecdotal evidence and only comes from a tiny dataset that we ourselves observed, but we think that A2M is in a great position to benefit from the rise of supermarkets in China.

The DOL channel much like the MBS serves not only as a marketplace but also a platform to advertise to consumers and utilise “showrooms” on digital platforms like Taobao where A2M can live sell to consumers – think Teleshopping - online. The two main digital platforms for A2M are Tmall and JD.com where they have their own digital stores and live “showrooms”. A2M has only a 2% market share in the DOL channel and see it as a key future growth driver. Online shopping trends are continuing to grow in popularity and there is a clear trend towards wealthier cities preferring to shop online. Going forward A2M’s target is to have a higher market share in DOL than they do in MBS. We think with the trends towards wealthier consumers choosing to shop online this is an area A2M must focus on gaining market share.

Despite the relatively low market share A2M’s products are highly desired and have had extreme success in Chinese online promotion days. Industry reports indicate A2M’s Tmall ranking during Alibaba Group’s 2021 Single’s Day promotion from November 1 to 11 improved to #2 within the infant formula category. More recently data from JD.com showed that on its 15th of April 2022 Anniversary day event, sales of imported baby products saw prominent growth, Aptamil, Nestle and A2M were the most popular infant formula brands with new parents. Finally, on 31st of May 2022 during JD.com cross-border event the top 3 brands in sales are Nintendo, Swarovski and A2M. In the past Chinese consumers have be wary of buying online due to the ubiquity of fake products, however as these platforms have developed and Chinese regulation has become stricter Chinese customers are turning to online marketplaces. A2M has done a good job of protecting its brand online, avoiding online platforms like PinDuoDuo which has a reputation for nefarious products. Finally in the aftermath of the pandemic A2M took actions to reduce channel inventory and replaced older inventory to improve inventory freshness, despite these actions the DOL segment seen 19% YoY growth in 2021 and we except that the company has a long run way ahead of it in this channel.

English & other label

English & other label did $523.9mm in sales in 2021, a decrease of nearly 52% from the prior year. Covid lockdowns had a devastating effect on cross trade and travel which are crucial for A2M’s English Label route to market. Covid restrictions were so severe in China that A2M were forced to cease their Hong Kong label with no possible route to market. The pandemic exposed A2M’s convoluted and opaque routes to market and A2M struggled to get a clear picture of market conditions causing a pile up of inventories and a denigration of inventory freshness. To protect brand integrity A2M swapped out old inventory with new and ultimately had to write down $58.3mm of English Label stock.

The ANZ segment contains both a substantial amount of liquid milk as well as IMF so we can only try to deduce EBITDA margins for English Label IMF. Historically, English Label IMF conservatively had EBITDA margins above 50% as there is very little distribution cost for these channels as it is mainly resellers. Moreover, in the English Label channel we have often seen that the resellers advertise the product, so for many years A2M has been able to grow without huge marketing spend because its resellers were doing the marketing for them. However, as the segment got hammered by Covid, EBITDA margins were almost cut in half to 26%.

The English Label segment has grown as Chinese consumers demanded high quality foreign products that they know aren’t fake. China has historically had a big problem with counterfeit products and consumers want to know that they are getting what they paid for especially with things they or their children will consume. However, as China modernises and regulations become stricter Chinese consumers are starting to put more trust in Chinese supply. Even before Covid consumers were shifting away from buying products from abroad to buying locally in China. Covid exacerbated the shift and the role these channels will play in the future is uncertain. Generally speaking there are two routes to market for the English Label products, Cross-border e-commerce (CBEC) and ANZ retail/Daigou/reseller

CBEC is similar to the DOL channel expect it deals with English Label products actually coming from Australia or New Zealand. Again A2M sees this as a key platform for advertising and brand building, utilising “showcases” on platforms such as Tmall, JD.com. CBEC includes authorised resellers as well as their own flagship stores. The CBEC route to market is generally quite complex and visibility in the channel has been a problem. To protect the brand it is also vital that customers aren’t getting counterfeits which can be difficult when A2M doesn’t have a great control over the distribution chain. However, the recent introduction of QR codes on tins has solved both these problems. With a quick scan of the QR code the customer can track where the tin has come from and A2M can track where tins are going gaining clarity in a very complex market.

A2M had a 21.1% market share in the CBEC channel despite revenues from the channel falling 51% because of the huge difficulties A2M faced getting products to the market while also trying to keep inventories fresh. One exciting opportunity A2M see in this channel is what they call Offline to Online (O2O) which is where they work with their retail customers in ANZ to set up their own stores and “showrooms” on Chinese platforms. CBEC is likely to see growth again as Covid restrictions disappear, and as A2M works with its retail partners to get more online stores promoting their product.

The Daigou/reseller/ANZ Retail (Daigou) channel is the most complex as often there can be multiple owners of the product before getting to the end customer. Included in this channel is ANZ retail sales a large part of which goes to China but a portion of the sales will be consumed in ANZ.

Daigou was born out of distrust for Chinese supply chains and counterfeits with Chinese customers willing to pay a premium to know that they were getting the real product from abroad. Daigou began as the “suitcase trade”, with Chinese tourists coming back from Australia or New Zealand with a suitcase full of product and reselling it. From there it has evolved into an interconnected and sophisticated network of resellers. For many resellers today this is their full time job and some have even built big businesses out of it. Resellers can be found on E-commerce platforms, open C2C networks like Taobao, closed C2C networks like WeChat and Offline to Online, which is usually ANZ retail stores that have an online store in China.

Daigou has been a critical factor in the A2M’s rapid growth as the resellers have been the most dedicated brand ambassadors promoting the brand on their stores and spreading A2M’s message. However, it is also the channel that has been most affected by Covid and while China continues to have very stringent restrictions in place the importance of the Daigou channel going forward is uncertain. In 2021 sales in the Daigou channel fell 52.1%. There are signs of recovery in the channel with Bubs an IMF competitor announced in Q2 2022 that sales from its Daigou channel was up 196% to above pre-pandemic levels. While we wait for A2M to announce its H2 results, we can take this as a good sign that the channel is recovering. As for the long term future of the channel, we think Daigou will continue to be a source of creating brand buzz but the shift towards China Label will continue with A2M needing to take greater responsibility for its marketing.

Liquid milk

A2M did $240.5mm in liquid milk sales in 2021. The vast majority of these sales, $169mm come from Australia where A2M has one of the highest market value share of 12.2%. The remainder of the sales came from China & Asia, $8mm and North America, $63mm.

A2M liquid milk sales in the Australian market are likely to grow slightly above the market, which is projected to grow at around 2% a year. We have seen A2M introduce new innovative products as well as take market share which has lead them to consistently grow faster than the market.

Greater China offers a huge opportunity for A2M to offer a premium milk brand in the 2nd, 3rd and 7th most expensive milk market in the world. Only recently has A2M introduced liquid milk into China, placing its product at the very top end of the category, with a litre of A2M typically costing 60rmb ($14.15), at least double the average price. We believe big opportunities lie ahead of A2M with the growth of premium-supermarkets like Olé. Liquid milk sales in China grew 143% from 2020 to 2021, all be it off a very low base. We think there will continue to be high paced growth in the region.

North America is a new market for A2M and one that holds great promise. The North American segment is currently still unprofitable delivering a $33.5mm EBITDA loss in 2021. There have been hurdles in entering the already mature North American market, with consumers not willing to pay the high premiums A2M originally set. A2M has shifted the North American strategy towards affordable premium price points and segment profitability. A2M have introduced innovative products into the North American market like their partnership with Hershey. From our perspective this was a step away from the luxury health and life brand that we see A2M growing into.

Nutrition

While still a small segment for A2M we see that is has huge potential for the business and we think it can leverage its brand across the nutrition market. We have seen A2M introduce prenatal nutrition as well as nutritional support for children. We believe that eventually A2M will have a wide range of nutritional products that will support consumers throughout their life cycle, the A2 brand at the heart of consumer health.

New Markets

A2M has started entering into new markets, primarily in Asia where milk prices are generally higher than elsewhere in the world. In 2019, A2M successfully launched Stages 1-3 IMF in Korea with an exclusive distributor YuhanCARE. At the end of FY21, A2M had a 3% market share of the South Korean IMF market ~3% in the South Korea IMF market. A2M are targeting Vietnam, Indonesia, Malaysia and Singapore as new markets. We think that Asia offers A2M fantastic opportunities to grow as the region grows in wealth and look to consume western products and find ways to express their newly found wealth.

In 2022 the USA is going through an IMF shortage and there is a chance that A2M can get the approval needed to start supplying IMF to the USA.

Outlook for Chinese and Global IMF market

There are important trends going on in the IMF market that we think will provide strong tail winds for A2M’s growth. The global IMF market is set to grow from US$59bn in 2021 to US$125bn by 2030. The IMF market is a rapidly growing market as woman across the world are joining the workforce and as the world’s population grow wealthier they will chose to provide their children with the best nutrition available.

The Chinese market is set to grow at an even more explosive rate as China is seeing an influx of women into the work force and career being of increasing importance to women. This growth is in spite of the dismal Chinese birth-rates. In 2020 China experienced an 18.1% decrease in births and a further 11.5% decrease in 2021. China have tried to encourage birth-rates by decreasing the cost to parents, especially the cost of education, and have implemented pro-birth policies, such as their new three child law. We think this trend to lower births will spur more spending on children as families with only one child usually have two sets of grandparents and two parents looking after them and combined salaries to give that child the best nutritional care valuable.

The Ultra-Premium category, growing at an expected 16.9% CAGR 2020-2025. Premium and ultra-Premium milk formula is the main driving force behind China's baby formula market. High-end brands put forward stricter requirements for quality and win more added value and a better reputation for the products. China are improving their regulatory system all the time and putting in place stricter quality controls that will weed out weaker players and drive the market up towards quality. Recently Premier Li Keqiang argued for “the strictest possible oversight and accountability” and “toughest possible punishment” in safeguarding food safety. In March 2021 China implemented two new food safety standards regarding IMF that come into effect in 2023. Finally, the first batch of infant formula registration certificates will expire in 2022, the second wave of IMF recipe registration will be quite competitive under new requirements.

We think that the new tough regulation benefits A2M as they have top class standards. Moreover New Zealand – China relations are very good giving New Zealand based companies a distinct advantage over competitors. New Zealand have recently upgraded their free trade agreement with China - “This means that by January 2024, New Zealand will have the best access to China for dairy products of any country,” Jacinda Ardern

Finally customers are choosing to consume trusted brands with perceived added benefits like organic or a2. According to the Global A2 Milk Market Research Report the global A2 beta-casein protein milk market is valued at US$1.23 billion with forecasted 13.5% CAGR growth and is estimated to read US$2.5 billion by 2026.

We believe A2M has a host of macro tailwinds at its back, and if A2M execute properly we think that there is a long runway ahead of high growth and sustained high economic profit margins.

Management

A2M is undergoing a big change in management. Geoffrey Babidge lead A2M from 2010, till 2018 when Jayne Hrdlicka came in as CEO, but abruptly left after only 18months in December 2019 when Babidge was reinstated as interim CEO. Babidge oversaw the growth of A2M and really transformed the company from a science focused dairy company into a brand focused nutritional leader. It is not easy for a business to adapt to new leadership after such a long-tenured and instrumental CEO. However, in February 2021 David Bortolussi stepped in as the new CEO, and although it is still early in his tenure we think he has already made some good structural changes and we believe he has the potential to be the next great leader in A2M’s journey.

David Bortolussi

Prior to joining A2M Bortolussi had made a name for himself at Pacific Brands, where he worked initially as CFO and then in 2014 was made CEO. Bortolussi was instrumental in the turn-around of Pacific Brands. In 2014 the company was crumbling under $700million of debt. Bortolussi sold off iconic brands, got the business into a fantastic position and ultimately sold the business for $1.1 billion to Hanes in 2016, only two years after taking the CEO role. Bortolussi comes highly regarded with a reputation for hard work and strategic prowess. According to some sources A2M were very lucky to hire him as he was tipped to get the top job at US based Hanesbrands but because of travel restrictions brought on by the pandemic this made it difficult for Bortolussi, who resides in Australia, to accept the job. So he ultimately accepted the CEO position at A2M.

Joining A2M in 2021 in the depths of the Covid crisis has not made it an easy start for Bortolussi, but he has already made structural changes and set out a recovery and new growth plan for A2M. We think that Bortolussi coming in at the time he did gives him a great opportunity to reset the business and mould it to suit his vision. Bortolussi has also not given investors specific earnings projections and has set relatively low goals, to dampen down expectations on him and the business. We think this will be a under promise and over deliver type of situation, to ensure Bortolussi gets his tenure off to a good start.

We have seen a number of personnel changes and company reorganisation already under Bortolussi. The biggest change has been the reorganisation of the Asia Pacific division. Rather than having one big division that over saw all of A2M’s key markets, A2M has split the division up into three business units, China, ANZ and international English Label. We think this will increase the focus on key markets that have very different consumers, and will increase focus on new markets with a dedicated international division. In 2022 alone we have seen four changes in the executive team including change in CFO with David Muscat being named as the new CFO. Muscat was the CFO of Pacific Brands when Bortolussi was the CEO. These changes could be seen as a negative sign of tension in the executive team or it can be seen as Bortolussi moulding the team around him and bringing in people he knows and trusts. We prefer the latter narrative.

The board

We think that there are signs that perhaps A2M might need some board refreshment. David Hearn has been the chair of the board since 2015, yet still resides in the UK where A2M no longer has any business. David Hearn also pushed for bonuses to be paid out in 2021 despite the terrible results, leading to 24.7% of shareholders voting against re-electing A2M’s chairman of remuneration committee Mr Burns. Moreover, there has been a public dispute between former CEO Ms Hrdlicka and Mr Hearn. Furthermore, Hrdlicka was able to liquidate her entire A2M stake within only three months of her starting in the CEO position netting $4mm. Hearn has said that this was a huge oversight by the board and have including provisions in Bortolussi’s contact. We think that Bortolussi’s current targets are well thought out and should provide him with the right incentives.

Risks

China concentration

One of the many risks facing A2M is the concentration of sales it has in China. If A2M was suddenly not able to do business in China because of regulatory reason; unable to reregister their IMF recipe it would be extremely damaging to A2M. Moreover, Chinese dismal birth-rates threaten the IMF market and is likely to increase market concentration, which means in the future A2M might be competing against companies with very large market share.

A2M is making efforts to expand their geography with some early signs of success in South Korea and North America. However, A2M is has tried before, A2M ventured into the UK market in 2012 but found the mature market didn’t offer great long term opportunities and decided to exit in 2021.

Litigation

A2M is currently facing two class action claims from Shine Lawyers and Slater & Gordon Lawyers. The allegations in both proceedings are similar – legal action on behalf of investors who bought shares in A2M between August 2020 and May 2021. During this period the company issued four earnings downgrades and an inventory write-down, while the shares fell 62%. However at the time the world was in the midst of the Covid crisis and there was massive uncertainty especially regarding international trade, which makes up a large proportion of A2M’s sales. Moreover, going through the 2020 A2M investor material it is quite clear that the company believed that there would be little disruption to their business and actually seen some positive impact on their business - “Estimated COVID-19 had a modest positive impact in FY20 on both revenue and EBITDA”. They obviously got it wrong, their supply chains were not transparent enough to see what was really going on, but they made a mistake instead of taking nefarious actions that warrant class action.

While we think that giving earnings guidance in the middle of a pandemic was foolish we think that A2M did their best to inform the market during a time when there was so much uncertainty and it was hard for the business to get a clear picture of market dynamics. They aren’t exactly the only business that wrongly predicted the impact of Covid and the inventory write-downs were necessary to protect their brand. If anything this action shows that A2M is willing to take short term pain for the long term benefit of the company. Although we don’t have any sort of specialisation in this area we believe the class action claims against the company are groundless and will not have a material effect on the company.

Competition

A2M already faces a lot of competition from IMF manufactures, competing against giants like Nestle, Danone and Abbott. However, these giants have come under slew of scandals and scathing attacks in recent years, with the latest scandal coming from Abbott who were forced to do a product recall in the USA. This news also spread to China were parents are fed up with the misbehaviour of the big international brands. This shift away from the big international brands has started to show up in their market share, with all of the big international brands losing market share in China from 2020-2021. This has given rise to smaller international brands that haven’t been tainted by scandal yet and that focus on providing the highest quality infant nutrition like A2M and Bubs.

In China there has been a rise in nationalism, exacerbated by the trade war started under the Trump administration. The offerings of the local brands tend to be in the lower price category and for now the consumers of local brands are not the same consumers that A2M are trying to attract. We think that the rise of nationalism disproportionately affects the big international brands and will create opportunity for A2M to grow their market share.

Finally the a2 milk category has had a wave of new entrants with many companies seeing the potential in this extremely fast growing market. We believe that consumers don’t buy into the A2M’s brand because of the science we believe they buy into a brand that they trust to provide nutrition to their families and beyond. This is not the first time A2M has faced competition in the past, competitors look to come in and replicate what A2M has done but find their efforts bear very little fruit because A2M is not a science that can be easily replicated, it’s a brand they have spent years building and have won the trust of families across China and Australia.

Reliance on strategic partnerships

A2M has built their business on strategic partnerships along the value chain. This has left A2M capital light and able to focus on building their brand. However, there is also a certain reliance on these partnerships and if any one of them should suddenly cease to do business with A2M it could leave A2M vulnerable. Generally A2M has long term contracts with their partners and often formed partnerships together to commercialise opportunities. We have also seen A2M take minority stakes in their partners, for example Synlait is one of A2M biggest suppliers, A2M holds a 19.8% stake. Finally, we are increasingly seeing A2M acquiring majority stakes or buying whole businesses which puts their capital light approach in jeopardy moving forward. However, acquisitions like the 75% controlling interest in Mataura Valley Milk gives A2M far greater control over their supply and are able to develop innovative new products in house.

Breast feeding rates

While all mothers know that breast feeding is the best thing for their baby it doesn’t always happen and mothers need high quality IMF to substitute. A woman may choose not to breast feed for a number of reasons including returning to work, or she might not be able to. Research done in 2014 found that the often sited statistic “only 1-5% of women can’t” is completely inaccurate and came from an old paper with a small sample size. More recent research done by Stube et al, have found that around 12% of woman will experience “disrupted lactation”, far higher than previously expected.

A study from the China Development Research Fund found that the rate of exclusive breastfeeding among Chinese infants within six months of birth is only 29%. Sadly the trend is that as countries modernise breastfeeding rates drop as women enter the workforce. Rates for exclusive breast feeding at 6months is 25% in USA and in the UK only 1%. We don’t see a rapid increase in breast feeding rates disrupting the IMF industry in China sadly we are likely to see an increasing reliance on IMF.

Valuation

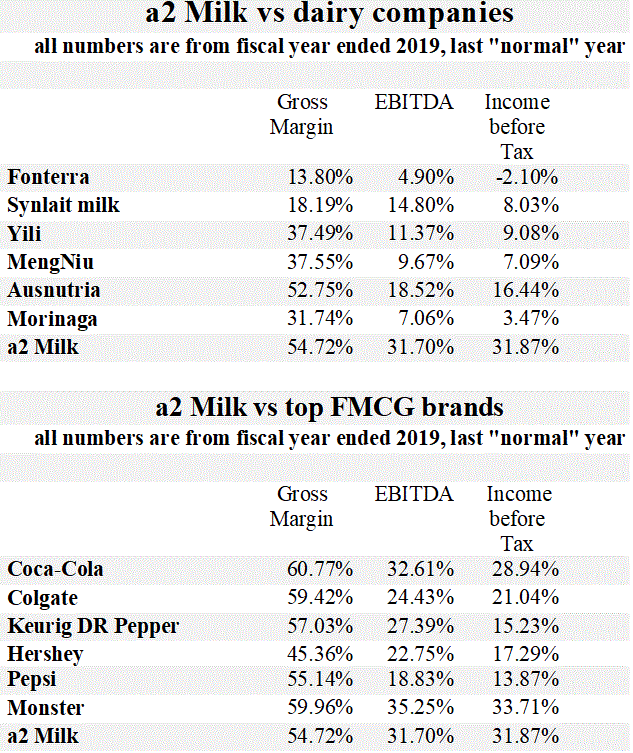

A2M had a terrible 2021 with total revenues falling 30.3% and EBITDA falling 77.6%. EBITDA margins were hammered with inventory write downs and channel mix, falling from almost 32% in 2020 to only 10% in 2021. A new CEO has been appointed who has stopped giving specific guidance and has set extremely low expectations. We think he is incentivised to set low expectations as he can come in and take credit for a far better than expected turn around. Moreover management is endowed with a horde of cash on A2M’s balance sheet making up around 22% of its current market cap.

We feel that we have been conservative throughout, including on the tax rate, we assume that A2M pays the higher end of their corporate tax mix 28%-30%. The discount rate of 10% is used in all of our discounted cashflows to provide comparable free cashflows and then we typically look for the share price target to offer a 50% margin of safety.

Despite the company focusing on EBITDA we have used a free cash multiple as we think this is suitable for this type of business. In this commentary we have provided an EBITDA multiple for comparison but we don’t find it very instructive.

In our Bear case we assume revenues take a long time to recover, with A2M not surpassing their 2020 revenue until 2025. EBITDA margins never recover, only ever getting to the very low end of managements targets. We also assume nothing comes of any of their new markets and no new products are introduced. In this scenario A2M grows well below the overall China Ultra-premium market and loses value share. This is an incredibly pessimistic outlook, yet there is still upside in this scenario. We think the terminal P/FCF multiple of 15x (9x P/EBITDA) well below industry average.

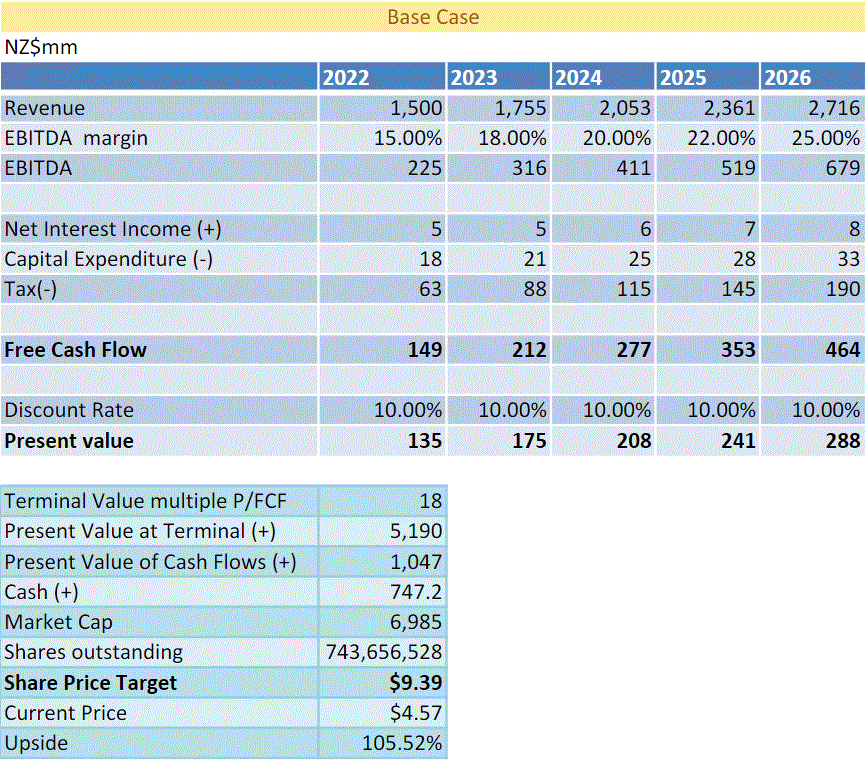

In our base case we assume that sales recover slightly faster with A2M surpassing 2020 revenues in 2023 and growing just slower than the overall China Ultra-premium market. EBITDA margins never full recover as A2M takes on more marketing spend and starts to vertically integrate lower margin supply into its business. An 18x P/FCF (12x P/EBITDA) is slightly below average for consumer stable.

We remain conservative in our bull case with a quicker rebound in sales, surpassing 2020 sales in 2023. Revenues rebound in 2023 but then growth falls in line with the Ultra-premium segment. EBITDA margins recover but never get to 2020 levels as A2M increases marketing spend and channel mix shifts towards China Label. To reach our bull case we still don’t ascribe any value to the new markets or new products but we do assume that the North America segment becomes EBITDA positive. In our bull case A2M would gain incremental market share, reaching their modest goals of 5% in China Label and 25% market share in English Label by 2026. We assign a slightly above average consumer stables P/FCF multiple of 20x (14x P/EBITDA), but well below the multiples ascribed to top FMCG brands like A2M.

Conclusion

In our opinion this is a highly mispriced compounder with a capital light structure. A2M is a top FMCG brand with a long run way for growth ahead of it. We think that sales will recover from the pandemic however the shift towards China Label is inevitable. A2M has many macro tailwinds at its back and if management execute right A2M could grow into a health and lifestyle brand that consumers trust to provide nutritional support throughout their lives. We have big hopes for new management but we are also wary of past mistakes by the board and are keen to see the massive amount of cash on A2M’s balance sheet put to good use. The market is currently pricing A2M as if it will never recover from the pandemic and is destined to be a low margin dairy manufacturer. We think this couldn’t be further from the truth, the brand is still strong and A2M is still at the beginning of its journey.

White Loch Capital Management is a fictitious fund used for educational purposes only

Thanks for reading

Email:whitelochcapitalmanagement@gmail.com

Twitter: @WhiteLochCM

Disclaimer: Do not interpret anything above as financial advice. This article has been prepared for informational & educational purposes only. The writing contains certain forward-looking statements and opinions which are based on the Author’s analysis of publicly available information believed to be accurate and reliable. While the Author believes that such forward-looking statements and opinions are reasonable, they are subject to unknown risks, uncertainties and other factors that could cause actual results to differ materially from those projected. As of the date the Report is published, the Author may or may not hold a position in the security mentioned. Nothing in this Report constitutes investment advice. Readers should conduct their own due diligence and research and make their own investment decisions. This is NOT a buy or sell recommendation.