Transact Technologies (TACT)

A misunderstood Good co/Bad co opportunity, with a solid underlying business and

Summary

· A small illiquid and misunderstood company

· Solid underlying business with a new fast growing recurring revenue business segment

· Management with skin in the game

· There is a catalyst for realisation of value in the foreseeable future

· The company has been caught up in the tech sell off in and we think it has created a great opportunity to buy

Graphs and images can be found in the PDF version of this article.

Disclaimer: White Loch Capital Management is a fictions fund that is used purely for educational purposes. The author uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. You are advised to discuss your investment options with your financial advisers, including whether any investment is suitable for your specific needs. Following publication, the Author may transact in the securities mentioned. All expressions of opinion are subject to change without notice, and the author does not undertake to update this report or any information herein.

Transact Technologies (Tact), Share price $4.24, Market cap: $42mm, 27/05/22

Executive summary

White Loch Capital Management thinks that there is potentially an opportunity in going long the shares of Transact Technologies. We believe that because of the wide market sell-off in small caps and money losing businesses, an opportunity exists in buying the shares of Transact Technology. We believe that this is a truly misunderstood business that optically looks like just another money loosing SaaS business. However, if you look under the hood of this business you will find a highly profitable casino printer business, a highly profitable QSR point of sale system (the legacy businesses) and a new SaaS business that is growing at high double digits and a huge addressable market. This is a classic Good co/ Bad co business where the market is completely focused on the money losing business and has forgotten about the years of steady profitability of the legacy businesses. Not only is this business materially undervalued there are two activist investors involved who have recently gained two board seats and we believe will pursue the sale of its legacy businesses, which we believe are valued substantially about the total market cap of the business today.

Historical business overview

Historically TACT was an international manufacturer of speciality printers primarily for the restaurant, casino & gaming, lottery and oil & gas printing market and point of sale (POS) systems. The company also offers maintenance & testing services, sells spare parts and consumables (labels, inkjet cartridges and other printer supplies) under the Transact Service group (TSG) segment. In 2019 management made the astute decision to halt the operations of its oil & gas and lottery business to focus on its more profitable and higher growth segments, including its new back-of-the-house BOHA! SaaS business.

The legacy businesses that remain relevant to today’s business are the Casino & gaming business that in 2021 accounted for roughly 39% of total sales; TSG accounting for 15% of sales and POS systems accounting for rough 12% of total sales. The new fast growing food service technology segment, which represents BOHA! accounting for 32% of sales.

Casino & Gaming

TACT primarily sells its Casino printers to manufactures of gaming machines (slot machines, video roulette machines), which traditionally would have used coins but now it is more common for these machines to use tickets and receipts. On the face of it this might seem like a commoditized manufacturing business. However, this is a highly concentrated market with Transact and Japan cash machine holding the majority of the global market share, roughly 80%. We believe the best way to think about this business is a niche manufacturer of an essential product, that without the slot machine itself is useless. This is a critical product to the slot machine OEMs who understandably prioritize reliability and often have long standing relationships with the printer suppliers. Arguably Transact’s Epic line of casino printers is the best in the business and comes with an impeccable reputation for reliability, according to Transact’s website the newest Epic Edge casino printer has less than 0.03% failure rate under the warranty period. Moreover, it is a very sticky business as often the printers are designed to fit specific machines and so the printers cannot be easily replaced by a different printer. The casino printer business is a cyclical business that provides lumpy revenue but we see this as a barrier to entry where many businesses prefer smooth earnings. As investors we would prefer lumpy earnings of $15 over smooth earnings of $10.

TACT also sells the industry leading software business to go alongside its printers where casinos can design different promotions and marketing tools that can be printed out on the coupons. Currently TACT is the only business to offer software that targets customers while they are playing updating the promotions as they are playing. We think that the software makes the business even stickier and really entrenches TACT in the heart of the casino’s marketing strategy. TACT not only gets recurring revenue from the software but also maintains strong relationships with its customers for labels and servicing which is generally stable and recurring.

The recurring revenue from the casino business is a sticky high margin business, we believe going forward the Casino & gaming business can command 50% gross margins and still has a long run way ahead. We believe that TACT has a reasonable moat in this sticky business and is a clear leader in the North American market with further room to grow internationally where already 30% of the segments sales come from. We believe that new entrants face high barriers to entry in this market, including regulation and tight-knit OEM relationships. Finally, we see some potential to expand its software business with expansions in consumer data, promotions and loyalty schemes that will help the casinos understand their consumers better.

Point of sale solutions

This business really started when McDonalds came to TACT unsatisfied with their current printers. While printers might sound like a commodity, in a greasy and hot work environment like restaurant they are typically very unreliable and there are safety issues around ink getting on the food. So TACT was tasked with designing a reliable printer for the restaurant environment TACT came up with the Ithaca® printer line which McDonalds was well received by McDonalds, who since 2008 has continued to use the Ithaca® printer. The fact that McDonalds had to approach TACT to design a printer for its restaurants tells us that it’s a tough market, where there is a lot of regulation. TACT has expanded its POS solutions outside of McDonalds but not meaningfully so. McDonalds still remains the dominate user of their POS solutions. We believe that the terminal is a commoditized product with little competitive advantage and operates in an extremely competitive environment. However, we do believe the McDonalds business is sticky as long as TACT maintains its reliability, and there is opportunity to cross sell to other restaurants where TACT already has a relationship. We believe this is probably a low margin business where the real money is made on the servicing and the consumables. TACT does not breakout gross margin by segments so this is a guestimate based on the information available

Transact service group

TACT offers consumables such as labels, maintenance services, ink cartridges and other consumables for its products. A big part of the TSG segment is spare parts and refurbished printers. For customer warranties to remain valid they must use TACT consumables. Warranties usually have a duration of 24months so there is some structural stickiness to TSG segment. Moreover, we believe that customers have little reason for switching for their printer consumables as often the labels and other consumables are specific to the printer. TACT does offer customisable labels and specialist labels like dissolvable labels. We think that this is a high margin sticky business where the inputs are a small part of the overall cost.

Food service Technology

In 2019 TACT launch its back-of-the-house BOHA! ecosystem that automates the back-of-the-house operations for restaurants, convince stores and food service providers. BOHA! offers cloud-based solutions for applications such as temperature monitoring of food and equipment, timers, food safety labelling, media libraries, checklists and task lists and equipment service management. The main selling point of the BOHA! ecosystem is that it streamlines operations through its series of apps and terminal, claiming to save 16 hours of labour per month for every location. There is a real need for the BOHA! solutions in restaurants and convenience stores today as food labelling requirements and food safety requirements get more and more stringent. Furthermore, there is ever increasing pressure on restaurants to cut food waste which the BOHA! ecosystem can help with. TACT also identified the shift to grab ‘n go meals in convenience stores and has focused on targeting convenience stores to help them to streamline and expand their fresh foods business.

TACT believes that the market opportunity for its BOHA! ecosystem is huge, with a TAM well over $1billion and more than 1,399,658 potential customers. Like the casino business the main profit driver from the BOHA! ecosystem will come from the recurring revenue, which is software, labels and other consumables.

The terminal itself costs $500-$800 and the expected annual recurring revenue per terminal is estimated to be $1000-$1200. Contacts are usually signed for 3years, however we don’t see reasons why many customers will switch away from the BOHA! labels and software after the 3years as the customer is unlikely to risk the functionality of the terminal for slightly cheaper labels. Having studied the competitive landscape we see that there are many similar offerings with many businesses having realised the opportunity. We don’t necessarily see this as winner take all market with space for multiple players to carve out a decent business. It is a relatively nascent market where we have little ability how the industry will look in 10years time.

Apple has chosen BOHA! to be part of iPad offering for restaurants. What this mean is that as Apple are trying to penetrate the restaurant industry and make the iPad ubiquitous in restaurant they will mention some of the applications available on the iPad, including BOHA!, and then they will share the information with the TACT sales team. It will also mean that the BOHA! apps are designed to work seamlessly on the iPad. TACT has designed the BOHA! Workstation to work with the iPad. We think this is a huge opportunity for TACT. It means if a restaurant purchases the iPad for its business operations it takes a lot of the upfront costs to the customer away from BOHA! as then they are really just selling the printers and the annual recurring revenue. We think this makes it easier for customers to choose BOHA! over competitors as the bulk of the upfront cost has already been spent on the iPad.

Where is the business today?

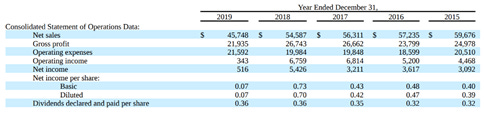

Transact Technologies was originally the printer business of Tridex Corporation and was spun-out in 1996. Since being spun out the business evolved little with some evidence of poor capital allocation and empire building. From 1996 to 2019, the share price has roughly stayed flat, and the business has managed to stay profitable in 18 out of the 23 years. Historically the business as whole commanded 40%-50% gross margins with volatile EBITDA margins around 10%. Since 2019 TACT has been undergoing a massive change in its business, discontinuing its business segments with low profitability and going from a profitable slow growth printer manufacturer to focusing its attention on its new fast growing Food Service Technology (FST) business. During 2021 TACT completed a public offering that raised net proceeds of $11.2mm with the purpose of using the proceeds to grow the BOHA! business. TACT has ramped up SG&A and R&D spending to focus on growing the BOHA! ecosystem, this has lead TACT to become an overall money losing business. The company and management have explicitly changed the mentality and direction of the business to that of a start-up. They have tried to refocus the business by cutting the dividend; changing management KPIs to focus on growing the FST business (eg, terminal installations) and hiring staff with software expertise.

It is fair to say that the outbreak of the Covid-19 pandemic affected TACT badly, casinos and restaurants both faced widespread closures globally. The business went into survival mode laying off 25% of its work force and taking a PPP loan that was eventually forgiven. Moreover, the launch of the BOHA! ecosystem was unfortunately quickly proceeded by the pandemic and so the growth of BOHA! was seriously impaired for a period of time. Supply chain disruption, chip shortages and labour shortages have continued to plague the rollout of the BOHA! ecosystem. However, the business has recovered well and we see a bright future for the BOHA! ecosystem and a strong recovery in the casino segment. There has been a clear demand for TACT’s products with the company finishing Q1 2022 with a record $13mm backlog across its businesses.

Casino & gaming

The casino business was hit especially hard from the pandemic as casinos around the world were forced to close. By year end 2020 sales in the Casino & gaming business had decreased by almost 50% to $11mm. We have seen a recovery in the Casino & gaming markets particular in USA and Europe whereas casinos in Asia particularly Macao have been slower to reopen. However, even as the world began to open the company was still faced with the problem of supply chain disruptions. TACT has manufacturing locations in China and Thailand which were plagued by Covid restrictions and transportation problems. However, we think the company has handled the sleuth of problems very well, implementing product workarounds and finding transportation alternative such as airfreight. In Q1 2022 we the casino business grow 66% YoY, and the outlook for the casino business is looking good with management saying that any product they can make has a customer, the bottleneck is supply not demand. We think long term the business will conservatively produce above 20mm of sales annually with high variance between the years. There is room to grow as the casino& gaming market grows and potentially new areas it can grow into with the marketing software. However, we also see risks such as replacing receipts with a QR code, we don’t have any evidence this is being done. However, it is conceivable that casinos could try to go paperless but that would also bring along its own problems and the fact the industry in heavily regulated we don’t see it being a big threat in the near future.

Point of sale solutions

Like the casino & gaming industry, the restaurant industry was hit hard with closures affecting multinationals like McDonalds as well as smaller restaurants. By year end 2020 the POS business had declined by roughly 35% to 3.8mm. In Q1 2022 the POS business rebounded about 12% YoY and the outlook for the business looks bright and the supply being the bottleneck. The recovery in the POS segment has also been hindered by part shortages with management saying McDonalds would take any printer they could make and that in H2 2022 POS sales will be roughly double that of H1 2022. Over the long run we expect that the relationship with McDonalds to stay and perhaps some cross selling to clients who are users of the BOHA! ecosystem. There are many competitors in this market, with Epson holding the dominant market position and we don’t see them taking any great market share. Moreover, management have been clear that their focus is on the FST segment and the casino & gaming segment and will deemphasize the POS segment. We think that the POS business could conservatively do 6mm annually with high variance between the years depending on the McDonalds replacement cycle and some potential upside from cross selling with its BOHA! clients. Valuation

Transact service group

Like all of the segments the TSG segment was also affected by the lockdowns and supply chain problems with sales from the TSG segment declining almost 30% by year end 2020 to roughly 7mm. In Q1 2022 we seen the TSG bounce back about 11%. However we are unlikely to see this segment return to 2019 level due to discontinued businesses and a move away from this segment to focus on the FST and Casino & gaming segments. We think that the business can conservatively do 8mm a year with a slow decline in the business as TACT focuses on its faster growing businesses. We also assume that this business has decent gross margins but are likely to decline over time.

Food service technologies

The BOHA! ecosystem was rolled out in 2019 right before the pandemic hit which slowed down its adoption. However, by the end of 2021 they had installed 9,818 terminals. The problems for the FST didn’t stop with the pandemic, chip shortages continue afflict the business. Q1 2022 seems to have been the peak in the chip shortages, with only 309 new terminals installed and management revising their guidance for new installed terminals in 2022down to 5,500 – 6,500 from 10,000. The demand for the product is clearly there as TACT have an ever growing backlog of over $13mm for the business as a whole. Our predication is that the worst of the chip shortages are behind us and the guidance for 5,500 – 6,500 new terminals in 2022 will end up looking incredibly conservative. We think that the business should still be able to make the 10,000 representing over 100% growth rate, with additional upside provided from its partnership with Apple which is still in its infancy. TACT recently held a joint event with Apple at the Chicago bears stadium. Moreover, the day after the Q1 2022 earnings, the company announced their biggest ever order of 140 BOHA! workstations. In the quarter the ARR for the terminals dropped down to $638 but the company is guiding for that to return the $1,000 - $1,200. While we are confident in managements that the ARR will return back to that $1,000 - $1,200 level it does show that the ARR isn’t exactly the best quality revenue and there is likely to be a lot of volatility in its earnings. Research has shown that there are still many competitors in this field, many of which have also struggled to source chips. While we think competition could be a problem in the future right now the business that BOHA! is replacing old systems like manual labelling and outdated filling systems. We have seen management really ramp up its spending on the FST business and while we are pleased that management is really getting behind the business, the cash burn of $7mm in the Q1 2022 has got us a little worried about TACT’s balance sheet. Management on the call was very candid and has initiated price increases that should be reflected in Q2 2022 alongside some cost cutting and dialling back on some of the investment in BOHA!. Despite wanting to see the BOHA! business expand we think that management is taking prudent steps to secure the balance sheet and get over this cash burn stage. The business does have a small $3.5mm debt line and still has $11mm of cash on the balance sheet which we believe used alongside the free cashflow from the legacy businesses, will be enough to take the business to where it is generating free cashflow.

Management

Bart C. Shuldman has been Chief Executive Officer and a Director of the Company since its formation in June 1996 and was the person leading the spin-off from Tridex. A number of the management team has been with the company since the spin-off in 1996 including president and CFO Steve DeMartino. The management team collectively own about 6.6% of the company the majority of the being held be the long term stalwarts Mr Shuldman and Mr DeMartino. From what we can gather management is very passionate about the business and despite not being its founder we get the feeling that Shuldman has a founder mind-set. One proof of this is that Shuldman has been willing to discontinue business lines and shrink the businesses to become more focused, we feel this goes against the normal of value-destructive empire building. Though we cannot be sure we assume that most of Mr Shuldman’s wealth is tied up in TACT and very much has skin in the game. Though the past performance of the shares has not been great, pretty much flat over since 1996, we believe that Shuldman is willing to learn new things and he has been very cooperative with the activist shareholders and genuinely seems to want the best for TACT rather than fighting off activists and keeping TACT as his personal fund.

Activists

There are two activist investors involved in the firm, Harbert Discovery Fund and 325 Capital who collectively own about 17% of the company. On March 2022, TACT entered into a cooperation agreement with the activists increasing the board from 5 to 7 seats and giving the two newly created seats to the activists. The activist investors have not stated publicly what their goals are but we assume that they will pursue the sale of the legacy businesses to create a singularly focused business with plenty of capital to capture the opportunity in front of the Restaurant Technology Service business. We think that a conservative value for the legacy businesses is worth substantially more than the current market cap of the business offering big upside from any sale. Moreover, even without pursuing any sale of the legacy businesses we feel more comfortable knowing that there are two activist investors involved with board seats that can hopefully guide management and steer them away from value destructive actions. One of the biggest risks in the thesis is dilution of ownership from a public offering as the management already has a shelf filling in place, but have been vocal in saying that they don’t intend to raise money from a share issuance in the foreseeable future. We think that with the activist investors on the board that a public offering becomes less likely and will hopefully steer management to internally fund the growth of BOHA!.

Risks

This is a small, reasonably illiquid, microcap where there are fairly large swings in prices, however we do not see this as a risk but an opportunity to take advantages of the low prices. There are a number of real risks to this business, many of which we have little opinion on such as – the rise of online gambling; potential technologies to replace gaming receipts; a downturn in the macro environment; further supply chain disruptions; further escalation from war in Ukraine the list is endless. However, there are some risks that we think pose a tangible threat to the business in the near term.

Liquidity

We think liquidity constraints and further public issuances pose the biggest threat to this investment thesis. The company currently has $11mm cash on its balance sheet and $3.5mm available under for loan. Prior to Q1 2022 we thought that TACT had ample liquidity and run way for cash burn. However Q1 2022 showed how an over eagerness from management to ramp up the FST segment alongside a tough macro environment and unfavourable timing of orders lead to a cash burn of about $7mm. This is clearly unsustainable. To combat this risk we think management will cut back spending and have already implemented price increases that should be reflected in the Q2 2022 numbers. Secondly we think there is a possibility of getting the revolving credit line back up the $10mm where it was in 2020. Finally, we think this will push management to spin off the legacy business realising value for shareholders and providing ample liquidity for the growth of BOHA!.

Competition

We think that the business operates in an extremely competitive environment in the Food Service Technology space, where there are many players offering similar products. We think that there are some switching costs mainly having to pay for the terminal again with relatively little gain from switching. Therefore, we aren’t worried about losing the customers we have at the moment but do realise that competition could hinder the growth of the BOHA! ecosystem. We also recognise that the whole industry is in a nascent stage switching over from old systems like labelling with pen and paper and outdated filing systems. We think that eventually the market will mature and then competition poses a bigger threat than it does currently. We think there is still a long runway for many players to carve out a good business.

Management

We think the loss of CEO Bart Shuldman or CFO Steve DeMartino would be a big loss for the business. They have both been at the business since its formation and it is likely in our opinion the Mr Shuldman sees this as his business and is the driving force of change to the FST segment. We also think if the legacy business was to be spun off that it could be a good opportunity to change management of the remain co to someone with more software experience. We have seen the business hire more people with software experience and we are encouraged by these recent hires.

Software

The software used for the BOHA! ecosystem is licensed from a third-party developer on a non-exclusive basis through 2031 and are subject to a revenue sharing arrangement with the developer. We see this as a huge risk and would like to see actions from management to secure the software and differentiate their product more. This reiterates that the FST is a largely homogeneous product with many businesses offering similar systems. Moreover, this leaves TACT vulnerable to the software capabilities and the integrity of their third party software developer. We do not think that software is BOHA!’s competitive advantage, we think that its high quality restaurant printers and its partnership with Apple are the real differentiators for the BOHA! ecosystem, yet we recognise that this isn’t exactly a strong “moat”.

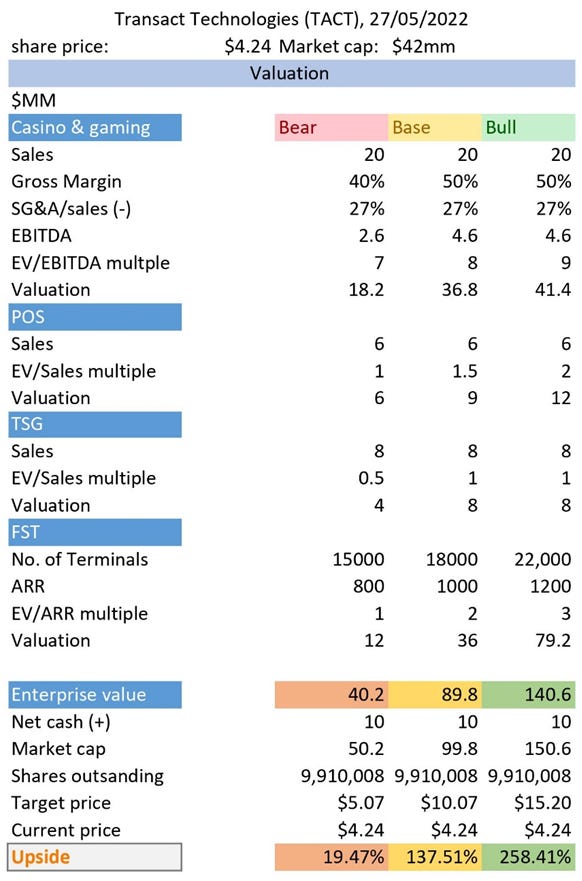

Valuation

The core of this thesis comes down to the unrecognised value within this business with catalysts already in place to recognise that value. We would very much classify this business as a “workout” rather a compounder that we see holding for many decades. Because the gross margins and profit margins of the segments are explicitly stated we have used what we deem conservative and crude metrics to come to our valuation. We think that there is a huge margin of safety in this business provided by the value of TACT’s defensible casino business. To stay conservative we used gross margin of 40%-50% however we think that the gross margin could likely be higher than 50% in its Casino & gaming business. We looked at the long run SG&A costs for the business as a whole and thought that 27% of sales was a fair number given the historic averages of the business.

Our assumptions for the FST segment are that management’s guidance for new terminal installations will turn out to be conservative as we see big upside from that guidance. We assume in our bear case that the business only manages to achieve the lower end of that guidance. In our bull case we assume that they only meet the upper end of their yearend 2021guidance, if supply chain shortages get worked out we could see installations top those number, so we again think our bull case is conservative. In our bear case we assume ARR does not get up to management’s guided number of $1,000-$1,200 range but remains substantially depressed at $800 per terminal.

For the POS and TSG segment we have just used crude EV/sales multiples. We do not have a clear insight into what they could be worth but we think that we have been conservative.

Conclusion

Transact Technology’s stock has been sold off alongside the rest of the tech industry. While the market is eschewing non-profit making companies we feel that the market has forgotten that TACT has a very profitable legacy business and has decades of profits to show for it. We think that there is huge upside in TACT’s stock and that there is already activist investors involved to help realise that value. We believe eventually the legacy businesses will be sold off and then the market will be able to properly value the Food Service Technology business.

White Loch Capital Management is a fictitious fund used for educational purposes only

Thanks for reading

Email: whitelochcapitalmanagement@gmail.com

Twitter: @WhiteLochCM

Disclaimer: Do not interpret anything above as financial advice. This article has been prepared for informational & educational purposes only. The writing contains certain forward-looking statements and opinions which are based on the Author’s analysis of publicly available information believed to be accurate and reliable. While the Author believes that such forward-looking statements and opinions are reasonable, they are subject to unknown risks, uncertainties and other factors that could cause actual results to differ materially from those projected. As of the date the Report is published, the Author may or may not hold a position in the security mentioned. Nothing in this Report constitutes investment advice. Readers should conduct their own due diligence and research and make their own investment decisions. This is NOT a buy or sell recommendation.