Q2 Letter

We share: some current thoughts; what it is we are trying to do; Update on our holdings and thoughts on a non-investment idea

Quarterly Letter, Q2, July 2022

The structure of this quarterly letter is that first, we will share some current thoughts. Secondly, we discuss what it is we are trying to do at White Loch Capital Management. Thirdly, we will discuss how our businesses performed in the quarter. Finally, as an appendix to the letter we have attached thoughts on a non-investment idea that we think is applicable to investing.

We highly recommend reading the PDF version of this article with graphs and images.

Commentary

The macro environment

“There are decades where nothing happens; and there are weeks where decades happen.”

― Vladimir Ilyich Lenin

So far 2022 has been a tough year for investors, the S&P500 fell about 20% in the first 6 months of the year. Consumer sentiment is close or at all-time lows and investors have every right to worry about present risks: the risk of recession; inflation at levels not seen in decades; the constant resurgence of a deadly pandemic that has already killed millions of people; a war in Europe and the apparent impending doom of climate change, and that’s just the headlines. We think that the cost of inflation to the economy is very real, and the cost to individuals even greater. Moreover, the central banks of the world seem be behind the curve and unable to control inflation without crashing the economy. We see the effects of central banks moving interest rates on economy growth as analogous to trying to push (stimulate) or pull (tighten) something on a rope. When central banks decrease interest rates, therefore, stimulating the economy it is like trying to push on a rope, the effects are minimal and the transmission of stimulation through the economy is slow. However, when the central bank increase rates, it is like pulling on a rope, there is a strong and immediate effect. We think the central banks are between a rock and a hard place, on one hand they cannot let inflation run away, on the other they don’t want to crash the economy and risk the jobs of potentially hundreds of thousands if not millions of people. We have no way of forecasting what is going to happen, we know that eventually there will be a recession but we don’t think we have any skill in predicting when it will happen. What we do know is that over long periods of time there will be recessions and bull markets and there will be high impact/ low probability events that will shock the world. Therefore, at White Loch Capital Management we don’t spend time trying to predict what interest rates or any other macro factor will do, we take a long-term view and spend our time looking for resilient companies that can weather any storm and perhaps even take advantage of any shocks to the system.

The fact that our companies have the capacity to suffer allows us to take the long-view. If our companies were dependant on financing or were unable to survive a bad year, we would be forced to think short term. However, we are looking to partner with top quality management in companies with capacity to suffer. For example, both a2 Milk and Gentex are currently sitting on large piles of cash with no debt, we do not worry about these companies needing to refinance or going out of business, all we need to worry about is if they will be able to take advantage of the downturn and put the cash to good use. This is a good worry to have. It is critical for us to partner with management who have the fortitude to take advantage of a crisis, who can ignore the fear and turn greedy when others are running for the exits. We think that there are few better partners than Nathaniel Rothschild, who is both CEO and Chairman of Volex, and has already shown incredible capital allocation abilities. We think that Rothschild with his newly increased debt facility, with over $100mm left in dry powder, will be able to take advantage of this downturn and invest for the long-term. Our ability to focus on the long-term comes from owning companies we know will be around for the long-term and that can take advantage of crisis.

Although our businesses operate in the macro environment and any changes to the macro environment very much affects their business, we feel that we have no ability to predict what will happen in the chaotic world we live in. We like to think of ourselves as “Macro-desensitized” meaning for the most part we can take the long view and completely ignore the macro picture, however, at a certain threshold the macro environment is affecting our businesses to the extent we have to sit up and take notice. For example, trends in Chinese birth-rates massively affect a2 Milk’s business, however, we believe that a2 Milk has a long way to go in gaining market share and has the tailwind of a rising middle class in China to offset the effect of low birth-rates, therefore, we don’t pay much attention to Chinese birth-rates, at least for now. Furthermore, we will never invest based on a predication of what the macro environment will do, however, it can lead us to omitting certain sectors or companies with exposure to certain sectors. An example of this is that we have believed for many years now that the Chinese housing market is in a bubble, that is just now starting to crack, we have eschewed any investment with exposure to the Chinese housing market because we would not know how the cascading effects of a crash would affect any company with exposure.

Part of investing in robust companies is that they should operate in industries where we think we can, at least roughly, picture what the industry looks like in ten years’ time and where we feel that the threats to our businesses are well known. An example of this would be autonomous driving for Gentex or wireless charging for Volex. In both cases we think that the threats to their respective industries are well known and far out into the future, giving our business that have capacity to suffer time to adapt to the new environment. For Gentex we already see them investing in technologies that can be used in autonomous vehicles and robo-taxis. This is the type of long-term vision that leads to a resilient company that can compound for many years. We tend to avoid industries where we don’t understand the biggest threats to that industry or where we cannot picture what the industry looks like in ten years’ time.

FOMO

“Be greedy when others are fearful, and fearful when others are greedy”

–Warren Buffett

Over the last three years we have seen some pretty spectacular moves in the market both to the upside and downside. In the short run the market is driven by human behaviour, where the cascading effects of herd mentality can lead to some pretty extraordinary moves, oscillating between extreme greed and extreme fear. After the bottom of the market in March 2020 we saw some companies go on parabolic runs to the upside, often with little fundamental backing. It was hard to avoid hearing about how much money some investors had made betting heavily, often with leverage, on “meme-stocks” such as GameStop or AMC. As long-term investors, we must not get drawn into the psychological bubbles of the market and we must stick to understanding the fundamentals of businesses and only invest when the market is providing an adequate margin of safety. We remind ourselves “This too shall pass” and above all we must avoid permanent impairment of capital. We do not partake in the fear of missing out (FOMO). We take the view towards our businesses as private owners that we want to own for very long periods of time. We only take notice of the markets when they are offering extreme valuations, extremely high valuations give us a fantastic entry point into a high-quality business that we want to own for long periods of time.

Just as we did not experience FOMO during the 2020/2021 bubble in SaaS businesses and “meme-stocks”, we are not currently experiencing FOMO watching the big moves that oil and gas companies are making. We eschew companies that we feel society actively distains earning an economic profit. We believe that eventually society rejects that which is not good for it. We prefer looking for companies that enter into Win-Win relationships and are a net benefit to society. The world is currently actively working against oil and gas companies earning an economic profit, the world’s best minds and most powerful governments are coming together to solve the issue of high energy costs. When countries such as Sri Lanka have riots in the streets and overthrowing the government because oil and gas companies are making it too expensive to live, we think the likelihood of earning long-term economic profits are slim. If we were to value an oil or gas company we would have to apply an extremely high “fade-rate” to take into account the likelihood of society forcing the total diminution of economic profits.

What is our game?

“The first and most important element is game selection.”

-Yen Liow

Rather than focussing on the noise and short-term mood swings of the market, we want to keep focused on playing our game. We adopt the mind-set of the chief capital allocator across the few businesses we own. The first principal we must adopt is the mind-set of an owner. Despite the fact that we own a tiny fraction of any of the companies we own, we think about the businesses as if they were our own private business, where we have partnered with management to run those businesses. As the chief capital allocator of our tiny business empire we must choose how much of our capital we are giving to each of the businesses (our portfolio weighting). An implication of this mind-set is that we see the balance sheets of our businesses as an extension of our own, meaning that if our businesses have large net cash positions so do we. Therefore, we don’t feel the need to have large cash positions at headquarters (in our portfolio). If we believe that we have partnered with the right management to run our business that during a market down turn, it is likely that, they will be able to allocate that cash to higher return investments than we would be able to.

As part of defining our game we also must define what is not our game. Our game is not to play “the greater fool game”. By which we mean, buying a much-hyped company or asset in the hope that someone, even more gullible than we are, is going to pay us a higher price for the asset than we did. When we make the decision to buy a company that is because we truly want it to be part of our small business empire and we think that we are buying the stream of cash flows that the business will produce at a discount to its present value. This also implies that we will not buy non-productive assets, we know how to value things, we don’t know how to price things. Non-productive assets such as, fine art, crypto currencies, gold, do not produce cash flows and therefore cannot be valued. They can, however, be priced by “experts” to determine what they think an intelligent buyer will pay for the asset. We have no such skill. We do not fish in the busy pond of over-hyped assets where everyone is trying to guess what other people will pay for that asset. We only fish in the small pond of companies where we think we can make informed and explicit assumptions about what the business and its cash flows from operations will look like over the next 5-10 years.

Shorting is also not our game. We think that short sellers do a great service to the world as they keep potentially unscrupulous management honest and expose those managements that have already dug themselves into a nasty fraudulent hole. However, from our perspective shorting has the opposite asymmetric qualities that we are looking for, it offers a maximum upside of 100% (if the stock goes to zero), and an infinite maximum loss. This asymmetric distribution of outcomes is not one we want to expose ourselves to. Furthermore, short sellers are extremely exposed to path dependency. If a short seller initiated a short position at $100, and in two years’ time the stock went to $0 it might look like a fantastic result, but not if the stock had gone to $400 before dropping to zero, most likely the short seller would be both bankrupt and right. The exposure to negative high-impact events from short selling is too great for us to risk. Therefore, we avoid short selling while applauding those that do.

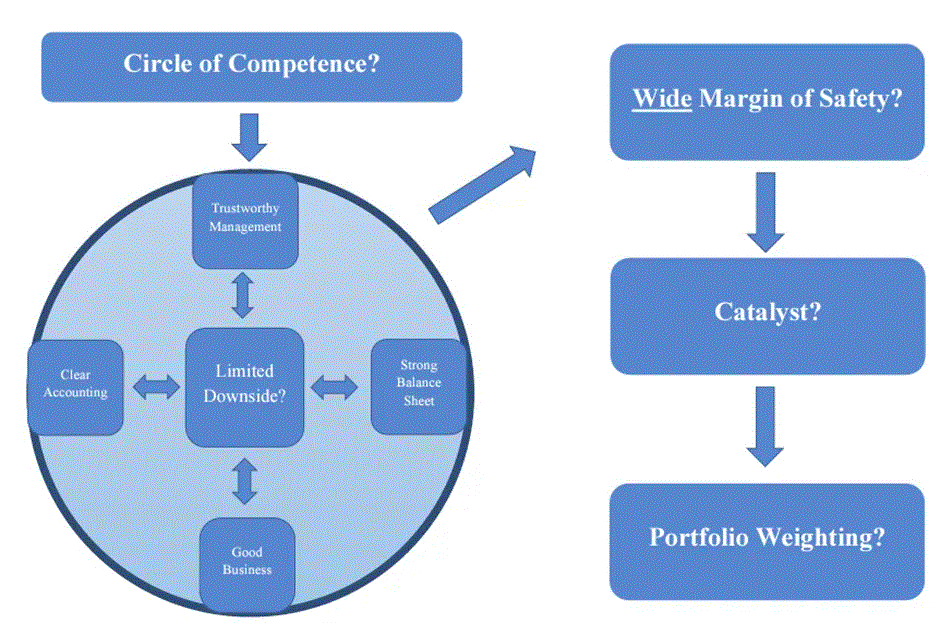

Our game is finding high-quality businesses led by management with integrity and finding asymmetric risk/reward opportunities with limited downside risk. We employ two investing frameworks, Compounders and Workouts. We have both frameworks in place so that we are able to take advantage of different opportunities that we come across in the market.

WLCM’s Compounders Framework

“10% of successful stock picking is picking great stocks. The other 90% is not selling them.”

-Ian Cassel

*These factors are directly linked with our Due Diligence Questions that we systematically go through when researching a company. For a more detailed look into what we are thinking about when looking at an investment please check out our “Due Diligence Questions” document.

We define Compounders as high-quality businesses with defendable completive advantages that allow the business to earn economic profits for a long time, led by management with integrity. If the business is good enough we don’t need outstanding management we just need them to be trustworthy and have the shareholders best interests in mind. For some compounders, such as Volex, management is a huge part of the thesis and the business would not necessarily be a Compounder without current management. When we think about Compounders we think in decades, and try to ignore the shorter-term volatility that is going to distract us from what is important. Often, we want to have a vision of where our Compounders will be in ten or more years’ time and we hope that management share that vision. Owning these types of high-quality businesses that have the capacity to suffer is what allows us as business owners to take the long-view over decades. When we go through periods where there seems to be incredible amounts of risk in the market we are thankful that we own assets that can endure through, if not benefit from, this short-term pain.

WLCM’s Workouts Framework

“Figure out what something is worth and pay a lot less.”

- Joel Greenblatt

*These factors are directly linked with our Due Diligence Questions that we systematically go through when researching a company. For a more detailed look into what we are thinking about when looking at an investment please check out our “Due Diligence Questions” document.

Workouts are extremely undervalued businesses where the potential distribution of outcomes is heavily skewed in our favour, we like to look for situations where “Heads we win big. Tails we don’t lose much”. We tend to require a catalyst or potential catalyst for unlocking value in a short time frame (short for us, 1-5 years). Furthermore, our key focus with workouts is limited downside, we do not want to enter into binary outcomes where we might lose our whole investment - our temperament isn’t suited for these types of investments. A perfect example of a Workout is Transact Technologies, it is a good business with no debt; management with insider ownership; recently activists having taken two board seats which serves as our potential catalyst and to round it off we think it is incredibly undervalued.

Ideally our whole portfolio would be made up of high-quality Compounders, however, Compounders are generally well known to the market and are very rarely offer at an attractive buying point. Moreover, Compounders are easier to recognise when they are already large and a lot of the growth is behind them, so it is useful for us to have a framework that can capture smaller undervalued companies that can potentially turn into Compounders. Once we have identified and bought an undervalued Compounder we intend to own it for life, unless something fundamental changes in the business. Our hope is that as time passes our portfolio will shift towards a portfolio full of high-quality Compounders that can grow our wealth with no further input needed from us. However, we believe that Workouts currently have a place in our portfolio because they help us broaden our universe of opportunities and they often move idiosyncratically, meaning that they don’t necessarily move with the market. We look for workouts that have potential catalysts for unlocking value within a short time frame, this usually means that the price of the stock will be determined by the catalyst unlocking the value rather than the short-term gyrations in the market. This can be psychologically beneficial. Furthermore, as investors with small amounts of capital we want to take advantage of our small size and look for mispriced securities in areas of the market where big funds can’t look. In small and illiquid stocks, we find more investments that fall under the Workout framework or at least not obvious compounders yet.

An update on our businesses

“Even the greatest stocks go through tough stretches. To endure is the price one pays for big winners.”

-Chris Mayer

We are always trying to take the long-view and ideally want to partner with good management for many decades. However, we must continue to be vigilant that management continue to operate with integrity and the fundamentals of the business are not retreating. We seek to strike a balance between giving our companies room to make mistakes and judging management’s promises and performance. We feel that when we buy a Compounder it is like a marriage, when we buy into the business our intent is to do so for life. Like a marriage we are willing to forgive small mistakes, but if we feel like we are constantly being misled by management or the company is constantly under preforming our expectations we need to track this so we can quantitatively say, over a long period of time that our choice of partner was probably wrong and the right thing to do is move on. For our Workouts because the expected time frame that we intend to own these businesses are shorter, 1-5 years, we need to be more ruthless and if we see that the thesis is starting to stray off track we need to sell the position and move on.

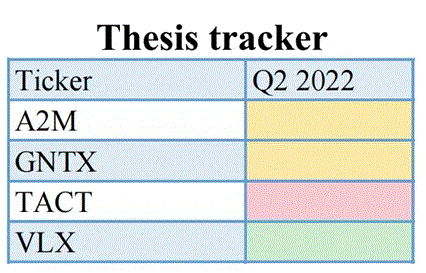

We use a quarterly tracker table to keep track of how we think the company performed in the quarter and to have a visual tool to track how our thesis is progressing. We do not only look at reported earnings we will also take into consideration industry developments and external threats and opportunities. We use a red square to indicate that events in the quarter deviated negatively from our thesis; an orange square to indicate that events in the quarter were either immaterial or roughly tracking our thesis well and finally, a green square indicates that events in the quarter deviated positively from our thesis. Moreover, we think this highlights the benefits of a well-informed DCF model when it comes to valuating a business, because we explicitly state all our assumptions we can easily track our assumptions and update them when they are inevitably wrong. We believe one of the main benefits to an explicit DCF model is the feedback loop it gives us, as investors, to learn and to track the evolution of a company.

· Red: Deviated negatively from our thesis

· Orange: On track with our thesis

· Green: Deviated positively from our thesis

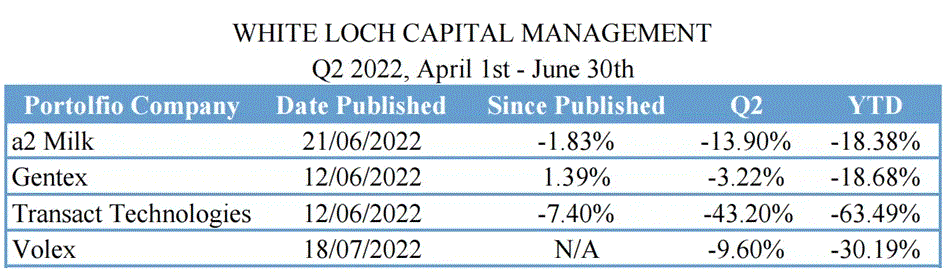

A2 Milk

Our ultra-premium infant milk formula brand, A2 Milk(A2M) didn’t report earnings in the quarter as they are only required to report bi-annually. A2M is heavily reliant on the Chinese market which during the quarter experience rolling lockdowns due to the pandemic. The main consequence of these lockdowns for A2M is that the Chinese ports became congested and imports into China slowed. We suspect that the worst of the supply chain crisis is behind A2M and we will see improved sales and inventory levels in August when the announce H2 results. Moreover, we expect that from here on out the opaquer channels to market, such as Daigou, will play less of a role in A2M’s mix, and that we are likely to see a greater focus on the China label, which means higher marketing spend but a greater control over brand image and better clarity in channel inventories. A2M is currently sitting on a substantial cash hoard and we will look to see how management is allocating that capital. We have been disappointed in management so far refusing to start repurchasing shares. We feel that cash levels are sufficient to support both investment in the business and buying back shares at, what we feel are, substantially discounted prices. Finally, we believe that one of the best defences of inflation is high gross margins and pricing power. A2M has both. Its high gross margins will help it absorb the cost pressures brought about by inflation whereas its strong brand image gives it substantial pricing power that will help lessen those cost pressures. We still remain very bullish on A2M and look forward to seeing how this relatively new management team will perform.

Gentex

Our rearview mirror and digital vision supplier Gentex (GNTX), had a good quarter announcing two more OEMs adopting their headline product, the Full Display Mirror (FDM). GNTX has had to operate in a tough light vehicle market over the past two years, with supply chains disrupting the manufacturing of vehicles. However, we feel GNTX has navigated this treacherous environment very well so far. Light vehicle inventories still remain close to record lows, we expect this to be a tailwind to light vehicle production and we should see elevated production levels in the latter half of 2022 and 2023 - even if a recession happens. GNTX has proved itself as the supplier of choice during this crisis, successfully redesigning products as they faced a continuous series of part shortages, causing minimal impact on OEMs. Moreover, GNTX delayed price increases to put pressure on weaker competitors. Despite cost pressures GNTX still retains a solid gross margin of 34.3% (down from 37.9% the year prior), and a net margin of 18.7%. Furthermore, GNTX’s large cash balance, which sits at over $280mm, allowed GNTX to repurchase 2.44 million shares in the quarter. GNTX’s high gross margins and large cash balance, alongside management with Owner-mind-set, give GNTX the capacity to suffer. During a period of time when many of GNTX’s competitors had disrupted OEMs production and were in cash-conservation mode, GNTX had the fortitude to deploy cash into growing the business and buying back shares at discounted prices. We think that GNTX’s high margins and efficient operations offers a great protection against inflation. Even if a deep recession is around the corner, the likelihood of which we have no view on, GNTX’s large cash balance will make sure that GNTX endures and emerges stronger out the other side.

Transact Technologies

Our back of the house software and slot machine printer supplier, Transact Technologies (TACT) had a tough quarter with a net loss of $4mm, $7.4mm cash burn and a reduction in Food service technology (FST) sales. Before this quarter the FST segment had been experiencing high double-digit growth, in spite of Covid, as they rolled out the new BOHA! ecosystem. However, during the quarter TACT was plagued by supply chain problems and restaurants being short staffed, which led to the drop in FST sales. Most frustrating of all was that the demand for TACT’s products was there but they were unable to fill the orders, finishing the quarter with $13mm in order backlog. As supply chain shortages ease up with expect to see that the demand for orders that TACT couldn’t fill in the quarter has been delayed and not lost. Since TACT announced its earnings in May they have announced several record-breaking orders from customers, we expect to see a bounce back in FST sales in their next earnings.

TACT has around $12mm cash remaining on its balance sheet. This clearly makes a quarterly cash burn of $7.4mm unsustainable. TACT has a debt facility of just $3.5mm, which is insufficient to help TACT survive with this level of cash burn for very long. However, there is evidence that this was just a bad quarter where the timing of sales and price increases led to an unusually high cash burn. TACT has implemented price increases that should be reflected in next quarter’s results. Moreover, management have announced that they will pause some of their R&D and marketing spending to address the current cash burn. Management have assured us that they have sufficient liquidity to sustain the business for at least the next 12 months.

Underneath the cash burn, is the highly profitable and stable Casino & Gaming segment which had a good quarter, growing 66% YoY, as casinos reopened from Covid closures. However, sales of Casino & Gaming printers were also castrated by part shortages, management said that customers were desperate for printers but they simply couldn’t fill the orders. While it is frustrating, TACT’s competitors were in the same position or worse, and to TACT’s credit they managed to redesign products on short notices to minimise the effects of part shortages. Like the FST segment we think a lot of the unfilled demand will be delayed rather than destroyed.

Despite this relatively bad quarter we think the drop-in share price has been completely unwarranted and now sits at, what we believe to be, a remarkable discount to intrinsic value. With a current enterprise value of $27mm we suspect that the whole business is trading at less than 5x this year’s Casino & Gaming segment’s EBITDA, giving the FST and other segments no value at all. We also think that it is likely that the FST segment will have around $17mm-$22mm of annual recurring revenue by the end of the year. To us this valuation makes no sense at all. At the start of the year two of the largest shareholders were given two board seats, which gives us a lot of comfort that there is someone looking over management’s shoulder and making sure the cash burn is controlled, which we believe it will be. We remain very bullish on TACT and take little notice of the current price as we believe this is a business that will continue to get more valuable over time

Volex

Our global integrated power solutions manufacturer, Volex announced very good full year results during the quarter. Volex’s revenues were up about 39% YoY, with more than 19% organic growth. Volex has positioned itself as a leader in electric vehicle grid cables and high-speed copper cables for data centres both of which are likely to continue to grow at very high rates in the future. We remain very impressed with managements capital allocation, with most internal investments returning the initial investment within two years. In the year Volex made 4 acquisitions paying an average, pre-synergies, EV/EBITDA multiple of 5.5 times. We think these are fantastic acquisitions that showcase managements price discipline for value creating inorganic growth. We see this acquisition strategy as a fly wheel, where management can acquire high quality companies that specialise in a niche but have been underinvested in, next Volex can inject cash into the business focusing on high return investments, then using the return from the investments to buy new businesses. Volex is still conservatively levered with more than $100mm in untapped debt facilities. We think Volex will be able to deploy this cash at very high rates of return during the market downturn that we are currently in.

The effects of inflation on Volex is minimal as it is industry standard to contractually pass through raw material and shipping costs to the customer. However, there is a lag when pushing through this cost and Volex reckons inflation accounts for a 1.3% drop in underlying operating margins. We think that Volex is a robust company with an owner-operator who is manically focused on continuous business improvement – Kaizen. Volex has already been a multi-bagger since Rothschild became CEO in late 2015, and we think it is well on its way to being a multi-bagger in the future.

Conclusion

“Over the long term, it’s hard for a stock to earn a much better return than the business which underlines it earns” – Charlie Munger

We believe that there are three types of advantages an investor can have, informational, analytical and behavioural/structural. We combine behavioural and structural together because investors can often not behave in a way that is beneficial to their returns due to the structure of their investment vehicle, we see the two as joined at the hip. At White Loch Capital Management, we are focusing on arbitraging human mis-judgment through, what we feel, are behaviour/structural advantages.

Firstly, when we invest in our Compounders we are truly in it for the long run, the ideal holding period is forever. We believe that overtime investors as a group can only earn what the underlying businesses can earn minus fees. It is true that, in the short run, prices will greatly fluctuate based on sentiment and the feedback loop effects of herd mentality, but we have no ability to predict these fluctuations. As long as we don’t over pay for a business in the long run we as investors will do as well as the underlying business. Therefore, we want to own the best businesses that can compound our wealth, at a high rate, over the long run.

Secondly, we use the structural advantage of our small size to hunt for short term (1-5 years), asymmetric opportunities, that offer a limited downside and big upside – usually found in small cap, under $1billion, where there is little to no analyst cover and the structural limitations of large hedge funds don’t allow for them to fish in this pond. We think that over time our Workouts will complement our Compounds well, as the Workouts with catalysts are likely to move idiosyncratically and provide us with a repeatable framework for generating returns.

Unless the world is really going to end, then history suggests that owning good businesses over long periods of time will generate a good return. We have no ability to predict what will happen in the economy or the markets in the short-term, but we are confident that our businesses will thrive no matter what the environment looks like. We think that if there was to be a deep recession our businesses would be part of the select few that come out the other side stronger. We are incredibly excited about the future, although the future will be fraught with difficulties and stochastic gyrations that will attempt to persuade us to act, we know that over time if we partner with the right people and don’t over pay for great businesses, patience will pay off. History is on our side.

White Loch Capital Management is a fictitious fund used for educational purposes only

Thanks for reading

Please contact us if you have any questions or want to discuss further anything we have written about.

Email:whitelochcapitalmanagement@gmail.com

Twitter: @WhiteLochCM

Disclaimer: Do not interpret anything above as financial advice. This article has been prepared for informational & educational purposes only. The writing contains certain forward-looking statements and opinions which are based on the Author’s analysis of publicly available information believed to be accurate and reliable. While the Author believes that such forward-looking statements and opinions are reasonable, they are subject to unknown risks, uncertainties and other factors that could cause actual results to differ materially from those projected. As of the date the Report is published, the Author may or may not hold a position in the security mentioned. Nothing in this Report constitutes investment advice. Readers should conduct their own due diligence and research and make their own investment decisions. This is NOT a buy or sell recommendation.

Appendix 1

Mise en place

Mise en Place is the French culinary phrase which means to “put in place”. Mise en Place is the culinary practice of diligently preparing and organising the ingredients and cooking environment before starting to cook. The practice encompasses: the chef understanding and knowing the recipe; preparing and arranging the ingredients, workspace and tools. This means that when the time comes to cook the chef is thoroughly prepared and is putting herself in the best possible position for minimising stress and the risk of something going wrong. Chefs will often standardise their Mise en Place process, producing a checklist to reduce the likelihood of forgetting to prepare something and increasing the risk of mistakes. The process of Mise en Place is where most of the chef’s work takes place, and the right preparation leads to the best chance of the right outcomes. Mise en Place can be taken from cooking and applied to other fields, with the same mentality of getting our preparation right to maximise the chance of getting a desired outcome.

Study/Writing/work

We think that Mise en Place can usefully be applied to studying, writing and work. According to research most people only get around 90-120 minutes of “flow-state” in a day. Flow-state is the optimal state of consciousness when people are able to focus and absorb information at a much higher level than is usually afforded to humans. If our goal is to maximise the chances of a good outcome during a bout of studying/writing or work then we want to put ourselves in the best position to capture this limited amount of flow-state that we are given. First, like the Chef we can prepare our environment, cleaning our workspace; perhaps turning on some Lo-Fi music and turning off our phones. Moreover, like the Chef we want to prepare our brains for the activity ahead, this could include writing down a little note related to the area we are studying or writing about the night before, letting our subconscious percolate the subject. Finally, as some Chef will standardise their Mise en Place, once we have found a process that has consistently led to good outcomes we can also standardise and document our preparation process.

Investing

The stochastic nature of investing dictates that investors are not able to consistently obtain desired outcomes, however with a consistent and proper process, the investor’s Mise en Place, investors can but themselves in the best position to maximise outcomes on the right side (gains) - and minimise outcomes on the left side (loses) - of the outcome distribution. Unlike the Chef, investors don’t have any hungry mouths to feed and can spend as much time on the Mise en Place as needed before any action is required - if the investor has structured her environment properly. The most successful investors spend almost all their time on Mise en Place, whether it is a quant refining and back testing models or an ardent, bottoms up, value investor who is spending his time reading and refining his investing framework. Doing the hard work of deeply understanding the businesses or strategies gives an investor the fortitude to stick with their chosen companies or strategies when Mr Market has chosen that those particular businesses or strategy is currently out of favour. Mise en Place is what gives an investor the courage to look like a fool in the short run and achieve successes in the long run.

Preparing the environment

For an investor to successfully execute their strategy they must first operate in an environment that will allow them to execute. Investors must resist the constant call from Mr Market to action and investors must only act when the research and preparation has been done. For some investors such as Warren Buffett and Guy Spier that means physically removing themselves from the noise of Wall Street and locating themselves in quieter locations, Omaha and Zurich respectively, where the environment allows them to spend a lot of time on Mise en Place without any pressure to act. Investors should also design their immediate environment to suit their investment strategy, for example in William Green’s “Richer, Wiser, Happier” it describes how Nick and Zak of the Nomad Funds had designed their office. Nick had a big desk full of books and the only computer in the office was a Bloomberg terminal on a short desk with no chair that according to Nick “you could only spend 5 minutes using the thing without thinking “oh my back is killing me””. Nick and Zak had fully mastered their environment to direct them to reading and away from looking at their portfolio and the enticing signals of the Bloomberg terminal.

Probably the most important way an investor will need to structure their environment will be how they structure their investment vehicle and the partners that they partner with. For an investor to be able to stick their strategy they must have the right partners who aren’t going to pull out their money when the market is down or when the investor goes through an inevitable period of underperformance. A way to achieve this is for investors to put their thoughts out in public and only select partners with a mind-set that is aligned with the investment philosophy. Finally, an investor can also structure their investment vehicle so that the partners are unable to act against the best interests of the investment vehicle, for example Warren Buffett’s Berkshire Hathaway gives him permanent capital. Moreover, investors such as Brent Beshore’s Permanent Equity have structured their investment vehicles to have a long equity lockup period, during which time the partners cannot pull their money.

Knowing the recipe

Like the Chef investors must intimately know and understand their recipe, whether that is having a deep understanding of the companies they own or having the belief in the empirical research that backs up their strategy. For us at White Loch Capital Management Knowing the recipe, means knowing the company reading annual reports, regulatory filings and news articles related to the business. It means knowing management, speaking to management, looking into past successes or failures of management and trying to insure we are partnering with high-integrity people. Finally, it also means understanding the wider business environment a company operates, competitor analysis, industry trends, regulatory trends, researching stakeholders up and down the value chain and we will do a Porter’s 5-forces analysis.

Standardising and documenting

Many investors choose to standardise their preparation with checklists or document their process via journaling. Once an investor is confident of their process standardising and help avoid biases, misjudgements and style drift. Due to the noise in investing it is often hard to get useful feedback to improve processes and frameworks, however journaling is a method investors can employ to get clearer feedback about their process – what was the basis for the investment decision at the time? What was the outcome? Was the process, right? Though journaling won’t be able to give an investor complete clarity it will help an investor get feedback about their investment process that they can learn from. At White Loch Capital Management, we are looking to take advantage of different opportunities and felt that a checklist structure is too ridged and felt that list of a due diligence questions to consider during the research process was more appropriate. Finally, we have found making public our investment theses and writing a useful way to improve our investment framework.